Agentic AI for Cross Selling in Banks: The Autonomous Revolution Transforming Revenue Growth

Agentic AI for Cross Selling in Banks: The Autonomous Revolution Transforming Revenue Growth

Banks have always known that the customers they already have are worth far more than the customers they have to acquire. The problem has never been data. It has been bandwidth, and the customer experience that bandwidth ultimately shapes for those customers. A retail bank with twenty million customers, fifty product lines, and a few thousand relationship managers simply cannot run a real cross selling conversation with every customer at the right moment, in the right channel, in the right language. Most banks already sit on rich customer data transaction history, account activity, life stages, spending patterns, credit history but moving that customer data into a timely, personalized conversation is exactly where the gap has lived. This is the change that finally closes that gap. It moves the bank from "we have an offer for you" to "the bank acted on your behalf, in the moment that mattered."

Why Cross Selling Is the Battleground for Banks in 2026?

Cross selling economics have always been generous for existing customers. Industry benchmarks repeatedly put the return on a cross selling motion at roughly ten times the return on acquiring new customers, and a five percent lift in retention across existing customers can push profit by twenty-five percent. That math has not changed for banks of any size, and it gets more powerful as banks layer agentic AI on top of their existing customers book.

What has changed is the competition. Fintechs and embedded-finance players are nibbling at every individual product line, from the credit card and debit card to the mutual fund SIP to the working capital loan. A traditional retail bank cannot defend its share of wallet from these new entrants in the financial landscape with quarterly campaigns and branch RMs alone particularly when many banks still run cross selling out of fragmented systems that were never wired together.

This is the backdrop against which agentic AI is arriving. As McKinsey notes in its retail banking research, the financial institutions that win the next decade will be the ones that make every customer interaction feel anticipated. Banks already hold the signals. The agentic operating model gives them the bandwidth to finally act on every one of them, turning routine cross selling in banking from a campaign motion into a continuous, customer-centric loop.

What Exactly Is Agentic AI, and How Is It Different from Generative AI?

It helps to be precise here, because the two terms get used interchangeably and the difference is the whole point. Traditional AI scores and ranks. Drafting models generate copy. Agentic AI acts on its own.

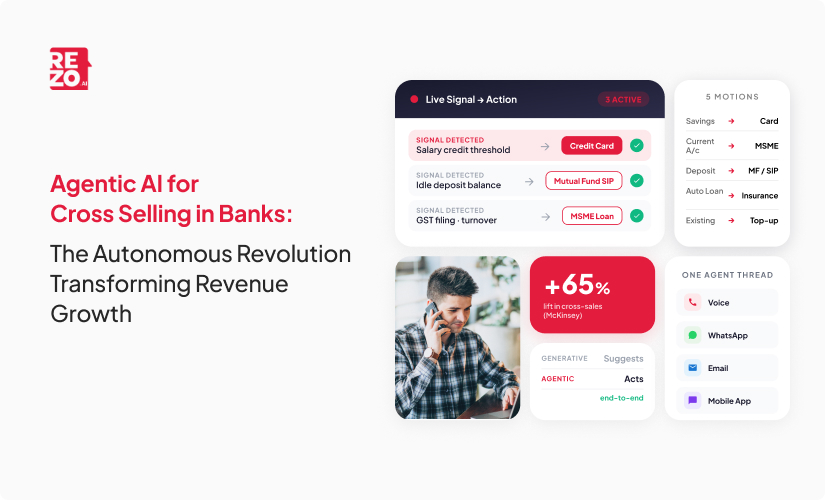

Generative models tell you what to say. Agentic AI decides what to do and does it. A drafting model can write an email about a credit card upgrade. An agentic system reads the signal that a salaried customer's spending has crossed a threshold, checks pre-approved eligibility, picks the channel the customer responds to best, opens a vernacular WhatsApp conversation, fields questions, captures consent, and fulfils the application end to end. As Salesforce summarises in its agentic AI guidance for banking, agentic AI systems perceive, plan, act, and learn. Unlike traditional AI that scores and recommends, agentic AI systems and networks of AI agents take action across multiple systems on the bank's behalf.

For cross selling, that distinction is everything. The bank does not need a smarter recommendation engine. It needs an autonomous teammate who can close an autonomous teammate that understands customer needs, reads the customer journey in real time, and knows when to act on behalf of existing customers and new customers alike.

Also Read: Agentic AI Voice Agents

How Does Agentic AI Drive Cross Selling Revenue in Banks?

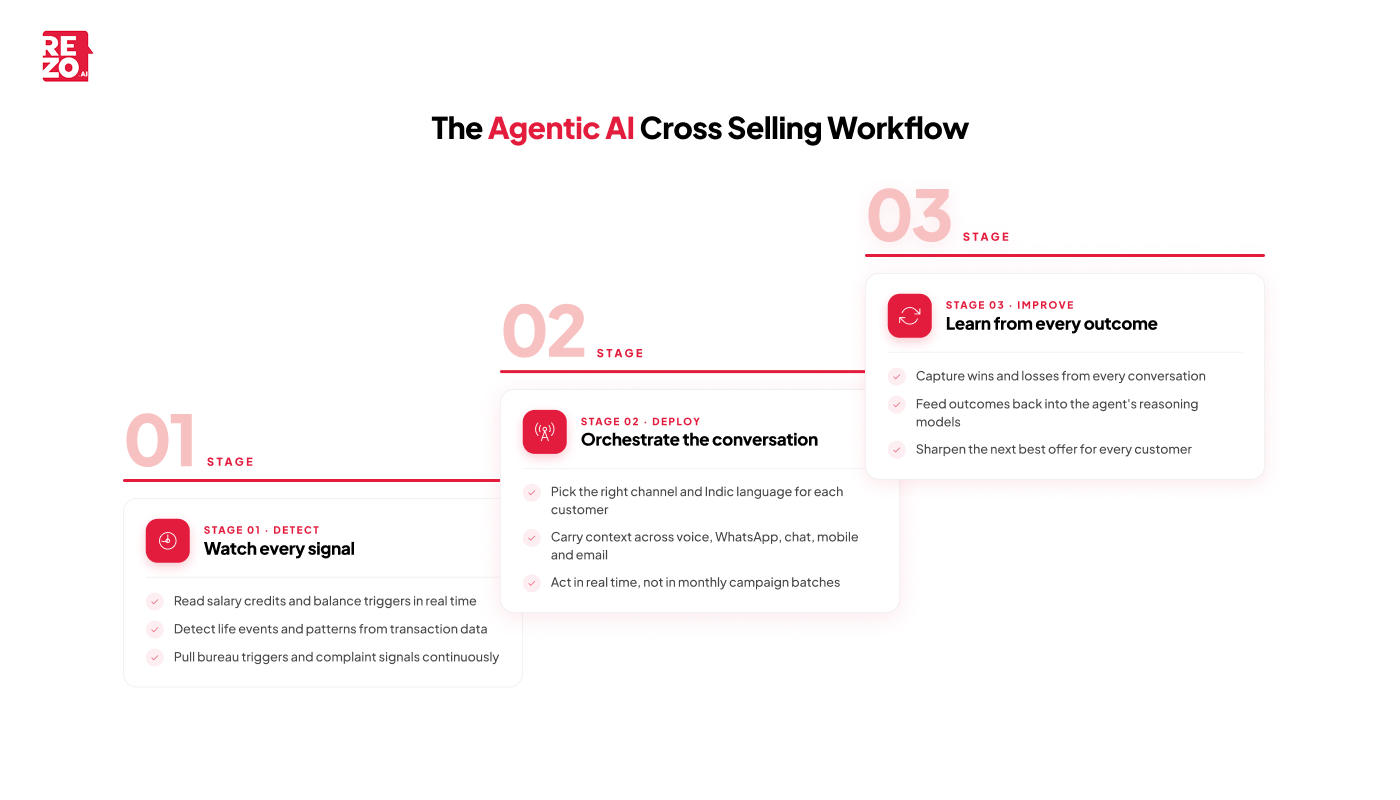

There are three moves an agentic system makes that a campaign engine cannot, and together they are how AI agents quietly take over the cross sell opportunities that used to slip through the cracks. This is essentially the economics of cross selling in banking flipped on its head moving every conversation from monthly batch to live signal, across millions of customers at once.

First, it watches continuously. Salary credits, idle balances, life events, complaint patterns, even bureau triggers from another lender are all inputs in real time, not in a monthly batch. The agent pulls from transaction data, account activity, customer feedback, and unstructured data sources like call transcripts and chat logs to build a live picture of every customer.

Second, it orchestrates the next conversation, on the right channel, in the right language, at the right hour, with full context. The same agent thread can run on voice, WhatsApp, chat, mobile banking, and email without the customer having to restart: a single continuous experience across digital channels that customers actually use, and across digital channels that financial institutions had previously struggled to stitch together for their customers.

Third, it learns from every closed and lost conversation, so the next best offer becomes genuinely better with every interaction. Customer feedback, win-loss patterns, and usage patterns all feed back into the agent's reasoning, so AI models tighten with every cycle and the bank moves from generic offers to relevant offers shaped around the right customer at the right moment.

McKinsey's banking research puts numbers on this. Banks that rewire a single frontline domain end to end are seeing three to fifteen percent higher revenue per relationship manager, sharper risk management on the assets side, and twenty to forty percent lower cost to serve, with early movers reporting up to a sixty-five percent lift in cross-sales and a thirty percent net annual growth in primary customers. A broader work on agentic AI in banking points to operational costs reductions approaching forty percent and a marked drop in operating costs as financial institutions automate complex tasks and absorb high volumes of routine outreach without adding headcount. These are not pilot numbers. They are revenue line items, and they show what changes for both the bank and its customers when AI moves from analytics to action.

Also Read: Agentic AI for Customer Service

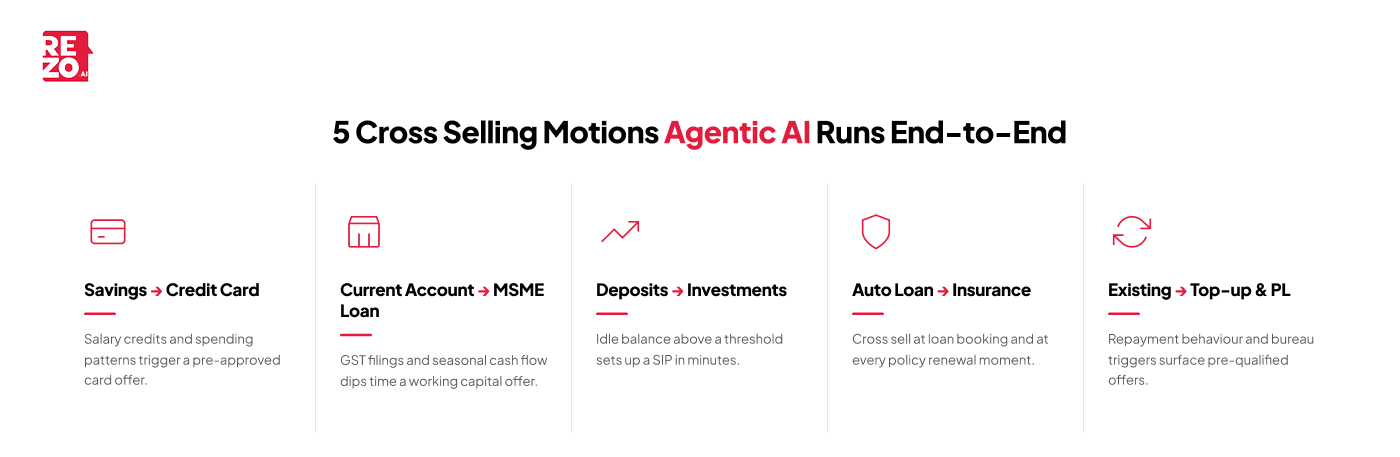

Five Cross Selling Motions Agentic AI Can Run End-to-End

Abstract is easy. Let's get specific. Here are five cross selling in banking motions where AI agents can carry customers all the way from signal to fulfilment and where the same agent layer surfaces fresh cross sell opportunities continuously rather than once a quarter.

Savings account to credit card. The agent watches salary credits and spending patterns on the savings accounts side for individual customers, then watches debit card and checking account behaviour for confirmation. When customers cross an eligibility threshold, a soft-pull check runs, a pre-approved card offer is generated, and a vernacular WhatsApp or voice conversation begins. Questions from customers on rewards, limits, and fees are handled inline. The card is dispatched without those customers ever logging into a portal.

Current account or checking account to MSME loan. GST filings, bank statement turnover, and seasonal cash flow dips become the signal. The agent reaches out at the right point in the cash flow cycle, explains a pre-qualified working capital limit, and, depending on ticket size, either fulfils the loan end to end or warm-hands over to a business banking RM with a fully briefed customer file. AI systems pull from filings, transaction patterns, and behaviour to time the conversation precisely.

Deposit balance to investment or mutual fund. Idle current and savings accounts balances above a threshold trigger an outbound conversation about investment products and broader wealth management options. The agent walks the customer through a short risk profile, reuses existing KYC, surfaces three suitable funds that align with the customer's financial goals across life stages, and completes the SIP setup. The first investment can be live in minutes, and the same flow extends naturally into long-tenure investment services, additional investment products, and education savings goals tied to specific life stages.

Auto loans customer to insurance. Cross selling here lives at two natural moments: loan booking and policy renewal. The agent runs a quick coverage review in the customer's language, compares add-ons in plain words, and binds the policy. Customers never feel sold to. They feel covered.

Existing customers to top-up, personal loans, or balance transfer. Repayment behaviour and external bureau triggers are the signal. A clean-paying customer with a competing loan elsewhere gets a pre-qualified top-up, personal loans offer, or balance transfer offer. The agent handles eligibility questions, captures consent, and pushes the disbursal end to end. The same logic surfaces other relevant banking products auto loans top-up, education savings plans, life-stage insurance wherever the customer's profile suggests they fit.

These five motions are not a finished list. They are the spine of a dynamic-bundling approach where agentic AI assembles bespoke combinations of financial products around individual customers' risk profile, life stages, and stated financial goals, rather than asking customers to navigate multiple products on their own. Customers see one curated set of choices, not a catalogue, and customers feel served rather than sold to.

Also Read: AI in Banking Customer Service

What Changes for Relationship Managers When Agents Join the Team?

The fear in every retail banking town hall is that AI agents replace RMs. The honest answer is more interesting. Agents replace the parts of an RM's day that an RM never enjoyed doing in the first place and the bits of the sales process where poor timing and human bandwidth used to lose deals.

Routine outreach, eligibility filtering, scheduling, paperwork chasing, and second and third follow-up calls are the bulk of an RM's calendar today. Agentic AI absorbs that. What remains is the consultative work, large-ticket investments, mortgages, MSME deepening, and recovery conversations that genuinely need a human read of the room. That is where stronger customer relationships are actually built, and where customer trust is earned over years.

The numbers back this up. Research shows the productivity uplift accruing to the RM, not against them. The RM who used to manage four hundred customers can now meaningfully cover two thousand customers, because the agent is doing the legwork between meetings and because the same agent layer handles routine queries from mobile banking, chat, and voice with personalized service for every one of those customers in their own language.

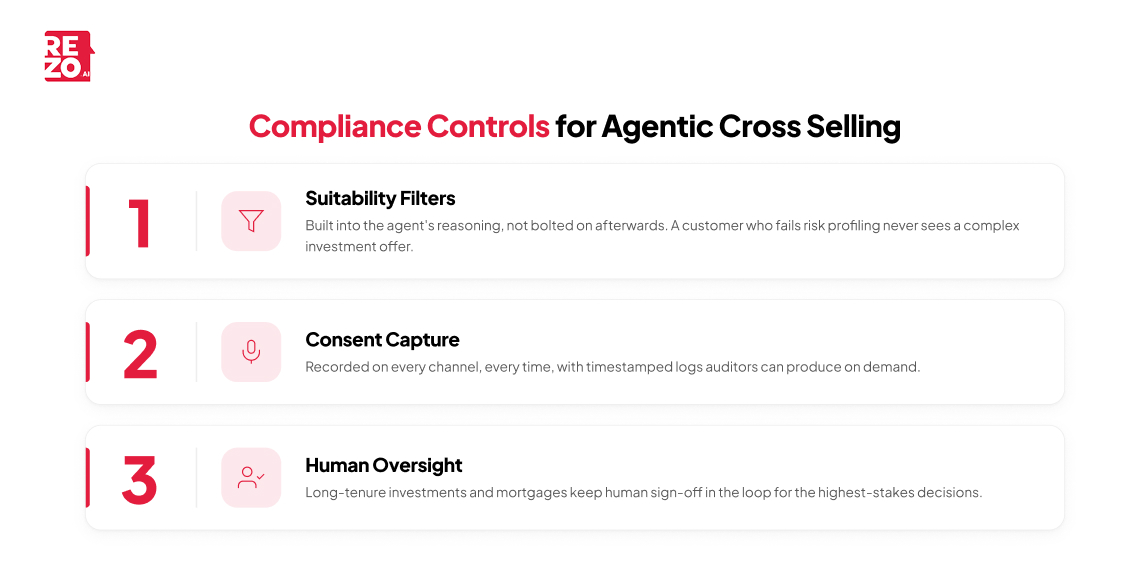

How Do You Cross Sell Responsibly? Compliance and Governance

Cross selling is a regulated activity. The mis-selling cases of the last decade are still fresh in every bank's memory and in the memory of the customers who were affected. Any serious deployment of agentic AI must answer to that history, which is why regulatory compliance has to live inside the agent rather than around it protecting customers and the bank in the same breath.

Three controls matter most. Suitability filters need to sit inside the agent's reasoning, not bolted on afterwards. A customer who fails risk profiling should never see a complex investment offer, regardless of how good their eligibility looks. Consent capture and recording need to run on every channel, every time, with timestamped logs that can be produced for any auditor. And the highest-risk products, particularly long-tenure investments and mortgages, must keep human oversight in the loop for the final sign-off light-touch human intervention exactly where the stakes are highest. The same agent layer continuously scans data for early warning signs of fraud or market volatility, which sharpens risk management and credit risk assessment without slowing the customer journey for everyone else.

Deloitte has been clear on this in its agentic AI in banking guidance: governance is not a separate workstream from the agent. It is a property of the agent itself. AI systems that handle live cross selling traffic have to surface their reasoning, log every decision, and remain explainable to compliance teams, business units, and operations teams alike so that customers, auditors, and regulators all see the same story.

Also Read: Agentic AI in Banking Operations

How to Implement Agentic AI for Cross Selling in Your Bank?

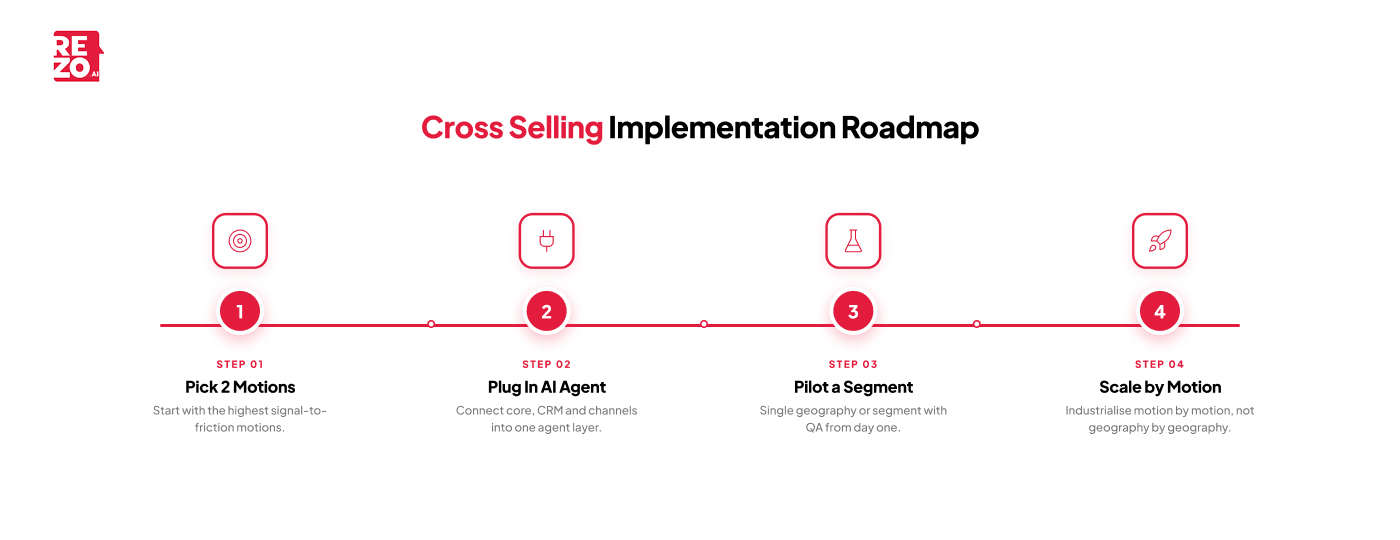

Most banks are not starting from zero. They already have a core, a CRM, a campaign tool, a contact center, and some kind of channel layer often spread across legacy systems and fragmented systems that were never designed to talk to each other. The right rollout is staged, not sweeping, and the goal is to scale AI safely on shared infrastructure rather than rip-and-replace the bank.

Step 1. Pick two cross selling motions with the highest signal-to-friction ratio. Savings-to-credit-card and idle-deposit-to-investment are usually the fastest to show movement, because the underlying customer data and trigger logic are clean and the customers being targeted are already engaged.

Step 2. Plug an Agentic AI CX platform like Rezo into your core, CRM, banking systems, and channels. The platform should orchestrate voice, WhatsApp, chat, mobile banking, and email natively, in Indic languages, with QA built in and connect cleanly into existing banking systems so a single agent can reach across systems without anyone re-keying customer data or making customers repeat themselves.

Step 3. Pilot in a single segment or geography, with analytics and call QA from day one. The early reads are not just on conversion. They are on customer experience, customer engagement, customer trust, and complaint patterns across customers in that segment and they tell you whether scaling AI further is safe, and how AI is actually landing with the customers it touches. This is also where many banks first see how AI changes the everyday experience for customers across digital channels they did not previously prioritise.

Step 4. Scale by motion, not by geography. Every cross selling motion you industrialise compounds the revenue engine and reaches more customers in the same calendar quarter. By the time you industrialise the fifth, the operating model has changed permanently and AI transformation has stopped being a programme and started being how the bank serves its customers every day.

Expert analysis of AI in financial services makes the same point at a higher level. Banks that treat agentic AI as a programme of motion-by-motion redesign get to value faster than those that buy a platform and hope. The right tools matter, but so does sequencing and operating costs come down only when AI agents are wired into the everyday workflow, not parked beside it.

Also Read: Agentic AI in Customer Journey Automation

The Autonomous Cross Selling Engine Is Already Here

Cross selling used to be a quarterly campaign. It is becoming a continuous, autonomous engine that watches every customer in real time, anticipates customer needs across the customer journey, and acts. Banks that build it first will earn a structural revenue advantage with their customers that is very hard to copy. Key takeaways for the leadership team are simple: the business value is real, the technology is here, and the institutions that wait will watch their best customers quietly migrate to the ones that did not. Identify customer segments where signal is strongest, pick two motions to industrialise, and let the agent layer compound from there across all the customers the bank already serves and the customers it will serve next year.

Ready to see what your bank's autonomous cross selling engine could look like, and what it could mean for your customers? Talk to our BFSI team at Rezo to map a roadmap that fits your customers and your portfolio.

Frequently Asked Questions

Will agentic AI replace relationship managers in banks?

No. Agentic AI absorbs routine outreach, eligibility checks, and follow-ups, freeing relationship managers to focus on consultative, high-ticket moments like mortgages, MSME deepening, and wealth management advisory. The model is augmentation, not replacement, with productivity uplift and stronger customer relationships accruing to the RM.

What are the biggest risks of using agentic AI in banking?

The main risks are governance blind spots, data privacy exposure, mis-selling, poor timing on outbound offers, and over-reliance on autonomous decisions. Banks mitigate these with suitability filters baked into agent logic, full consent recording, human oversight on high-risk products, machine learning models trained on clean transaction history, and continuous QA across every conversation.

How is agentic AI different from a chatbot?

A chatbot answers questions. An agentic AI system perceives signals, plans actions, executes across multiple systems, and learns from outcomes. For cross selling, that means the difference between offering a product to customers and autonomously closing the sale end to end, in the customer's language and channel with the agent reading account activity, usage patterns, and customer needs to act at exactly the right moment for each of the customers it serves.

Frequently Asked Questions (FAQs)

Take the leap towards innovation with Rezo.ai

Get started now