AI in Debt Collection: Transforming Recovery While Improving Customer Experience

AI in Debt Collection: Transforming Recovery While Improving Customer Experience

The debt collection industry is experiencing a profound technology-driven transformation powered by artificial intelligence. For decades, debt collectors and collection agencies relied on traditional methods like manual effort, repetitive phone calls, and one-size-fits-all approaches that often damaged customer relationships while consuming enormous resources. Today, AI in debt collection is reshaping how financial institutions approach debt recovery, delivering a rare combination: better business outcomes and improved customer experience.

If you are leading debt collection operations at a financial institution or managing debt recovery strategies at a collection agency, you have likely noticed the mounting pressures. Outstanding debts and delinquent account volumes are rising, operational costs are climbing, and consumers increasingly demand digital-first customer interactions. The question is no longer whether to adopt AI technologies for debt collection, but how quickly you can implement AI solutions effectively.

Why AI Matters in Debt Collection

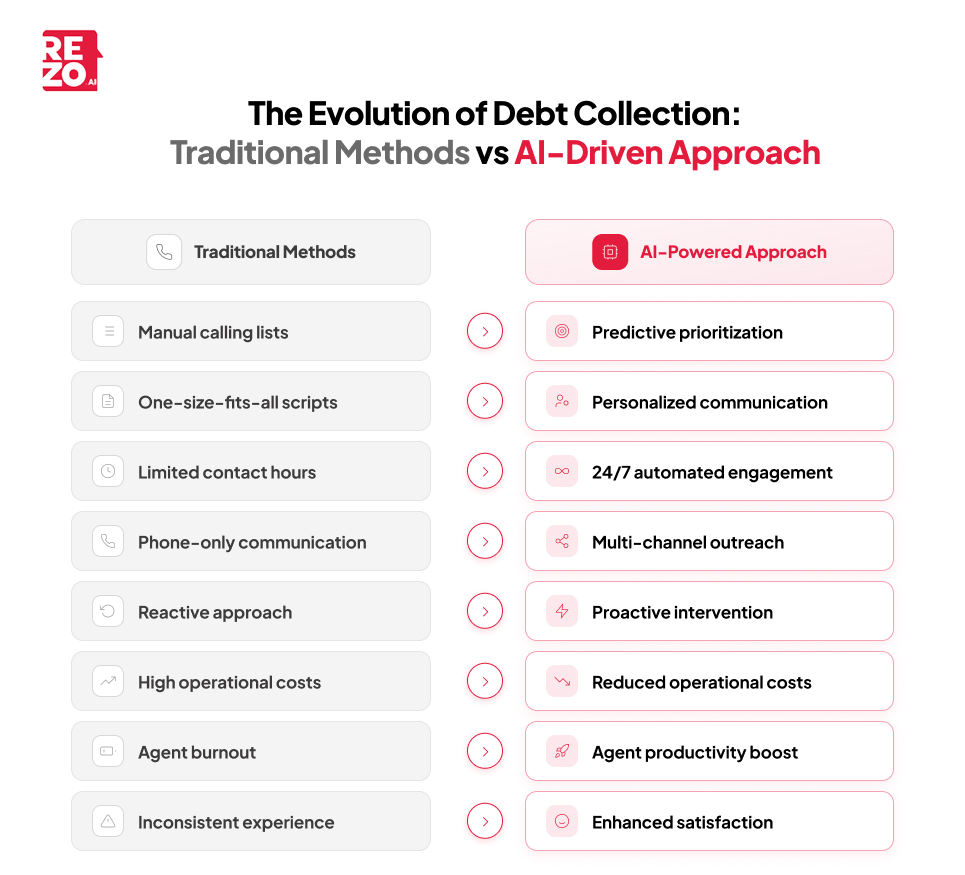

The traditional debt collection model is fundamentally broken. According to industry research, manual collection processes consume approximately 30% of collection departments’ resources, creating significant operational inefficiencies. Meanwhile, consumer expectations have shifted dramatically. The same McKinsey study found that 74% of consumers now prefer digital interactions through multiple channels over traditional phone calls when dealing with financial matters.

This disconnect between operational approaches and customer preferences creates a strategic vulnerability for the debt collection industry. Collection agencies and financial institutions face a difficult choice: continue with resource-intensive traditional methods or embrace AI technologies that can fundamentally change the economics of debt recovery.

The momentum toward automated debt collection is unmistakable. Industry data shows that 11% of debt collection companies were using AI systems in 2023, a figure that rose to 18% by 2024. Meanwhile, latest projections state that by late 2025, over 70% of financial institutions will be utilizing artificial intelligence at scale, up from just 30% in 2023.

What is driving this rapid adoption of debt collection automation? The answer lies in the tangible business outcomes organizations are achieving. Early adopters are not just experimenting with AI tools, they are seeing measurable improvements in recovery rates, operational efficiency, and customer satisfaction. For organizations still relying on traditional methods, the competitive gap is widening as AI driven automation transforms collection processes.

This shift also aligns with broader trends in customer service automation, where AI-powered systems are becoming the standard for managing customer interactions at scale.

Key AI Applications Transforming Debt Recovery

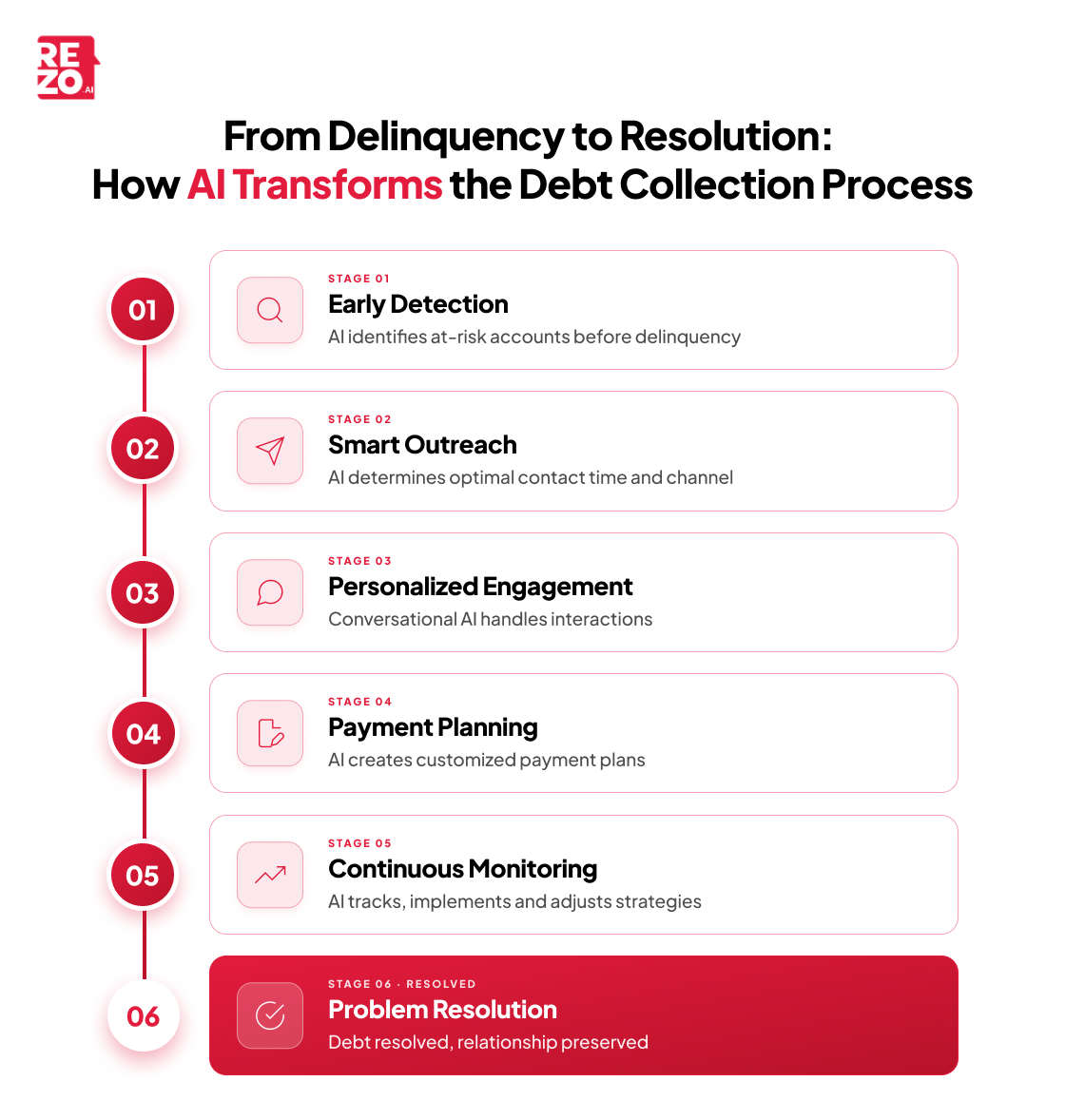

Artificial intelligence is not a single technology but a collection of AI technologies and advanced technologies that work together to optimize debt collection operations and improve the debt recovery process. Let me walk you through the most impactful applications across debt collection strategies.

Intelligent Communication and Engagement

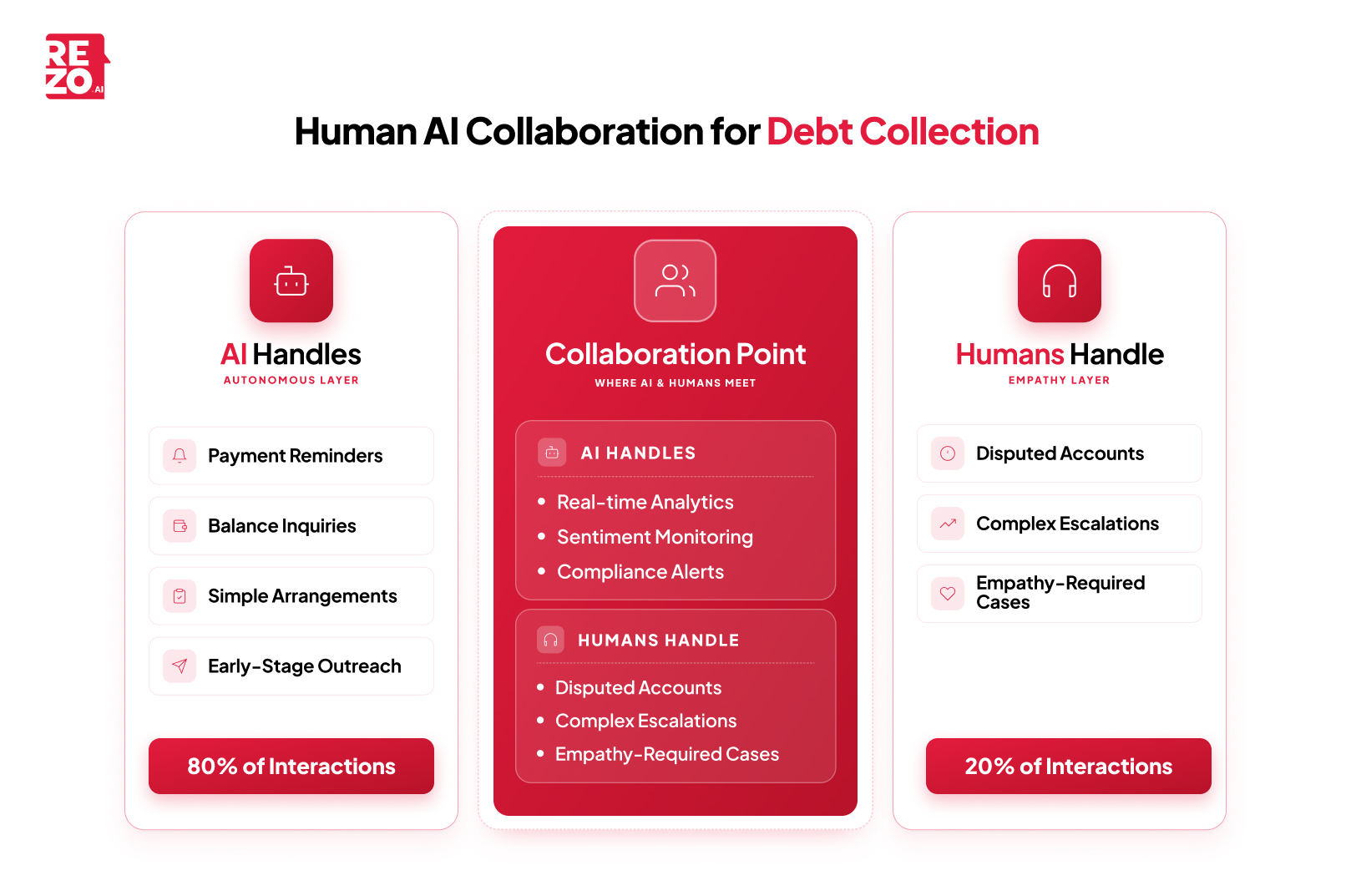

The most visible application of AI in debt collection is conversational AI, which enables personalized communication across digital channels using natural language processing. Rather than relying solely on phone calls, collection agencies can now engage customers through their preferred channels: SMS, web chat, email, or messaging apps with payment links and access to payment portals.

Gartner research indicates that by 2025, AI agent chatbots will handle 75% of customer interactions in debt collection processes. This is not about replacing human agents and debt collectors entirely, but rather about using AI systems to automate processes like routine tasks, payment arrangements, and account updates while freeing human agents to focus on complex cases requiring empathy and human intervention.

The distinction between AI agents and chatbots is important here. Modern AI agent systems can do more than follow scripted conversations. They can understand context through sentiment analysis, access payment history and customer data, and make decisions about payment plans based on individual circumstances and borrower behavior. These AI systems also provide right party contact verification and can analyze debtor responses to ensure effective communication strategies.

Predictive Analytics and Risk Assessment

Behind the scenes, AI models excel at analyzing patterns and predicting outcomes through predictive analytics and data analytics. In debt collection, this translates to smarter prioritization using behavioral insights and more effective collection strategies that prioritize high risk accounts.

According to Forrester’s analysis, AI technologies such as machine learning and predictive analytics are enhancing the collection process by assessing at-risk payments and forecasting debt recovery. Companies are leveraging predictive models to tailor debt collection strategies based on individual debtor profiles, payment behavior, and debtor risk assessment.

The results speak for themselves. According to ""Artificial Intelligence and Debt Collection: Evidence from a Randomized Field Experiment" by Yijun Zhou, algorithmic calling decisions achieve 23.4% higher repayment rates compared with human agents making those same decisions. AI systems do not get tired or experience human error, do not have unconscious biases about which high risk accounts to prioritize, and can process thousands of data points to determine the optimal time, channel, and approach for each account in the debt recovery process.

Industry data shows that 57% of AI adopters are using these systems to predict and segment accounts as well as predict payment outcomes and analyze payment behavior. This moves debt collection from a volume-based operation to a precision-driven one with data driven insights about debtor behavior.

Automated Workflows and Operations

AI solutions excel at automating repetitive tasks that previously required manual effort and human intervention. Payment reminders, automated reminders, follow-up communications, and even personalized payment plan generation can now happen automatically through debt collection automation, triggered by specific conditions or timeframes.

The efficiency gains from AI driven automation are substantial. Organizations implementing automated debt collection report 8x faster operations and 2-4x growth in collector productivity. This is not just about doing the same work faster through AI tools. It is about enabling collection operations to scale without proportionally increasing headcount while collections teams focus on strategic debt resolution.

These capabilities tie directly into broader contact center automation trends, where financial institutions across industries are discovering that intelligent automation improves both operational efficiency and service quality in the collection process.

The Business Impact: Real Results from AI Implementation

The business case for AI in debt collection rests on three pillars: operational efficiency, debt recovery improvement, and customer satisfaction. Let us examine each through the lens of real-world outcomes from financial institutions and collection agencies.

- Operational Efficiency: According to McKinsey’s research, generative AI in debt collection could slash operational costs by 40%. This comes from reducing manual effort, optimizing resource allocation through AI systems, and improving first-contact resolution rates. When you consider that traditional methods and manual collection processes currently consume 30% of departmental resources, the operational efficiency opportunity is enormous.

- Recovery Improvements: The same McKinsey study projected a 10% increase in debt recoveries with AI implementation. Separately, another independent research found that AI-driven predictive models and collection strategies improved recovery rates by an average of 25%. These are not marginal improvements in the debt recovery process, they represent millions of dollars in recovered debt and improved debt resolution for large financial institutions.

- Customer Satisfaction: Perhaps most surprisingly, artificial intelligence is improving how customers experience debt collection. Deloitte’s research found that organizations implementing agentic AI systems report 35% higher customer satisfaction scores compared to those using conventional automation. McKinsey’s data shows a 30% boost in customer satisfaction when AI technologies are properly implemented.

Why does AI in debt collection improve customer experience?

Because it enables personalized communication and convenient customer interactions on customers’ terms. Instead of disruptive phone calls at inconvenient times, customers can engage through digital channels and payment portals when it suits them. Payment plans can be tailored to individual circumstances based on payment history and borrower behavior. Communication strategies can be respectful and solution-oriented rather than aggressive, using engagement strategies informed by sentiment analysis.

Organizations using data-driven decision making in their debt collection strategies are finding that AI provides the data driven insights needed to balance debt recovery goals with customer relationship preservation through a customer centric approach.

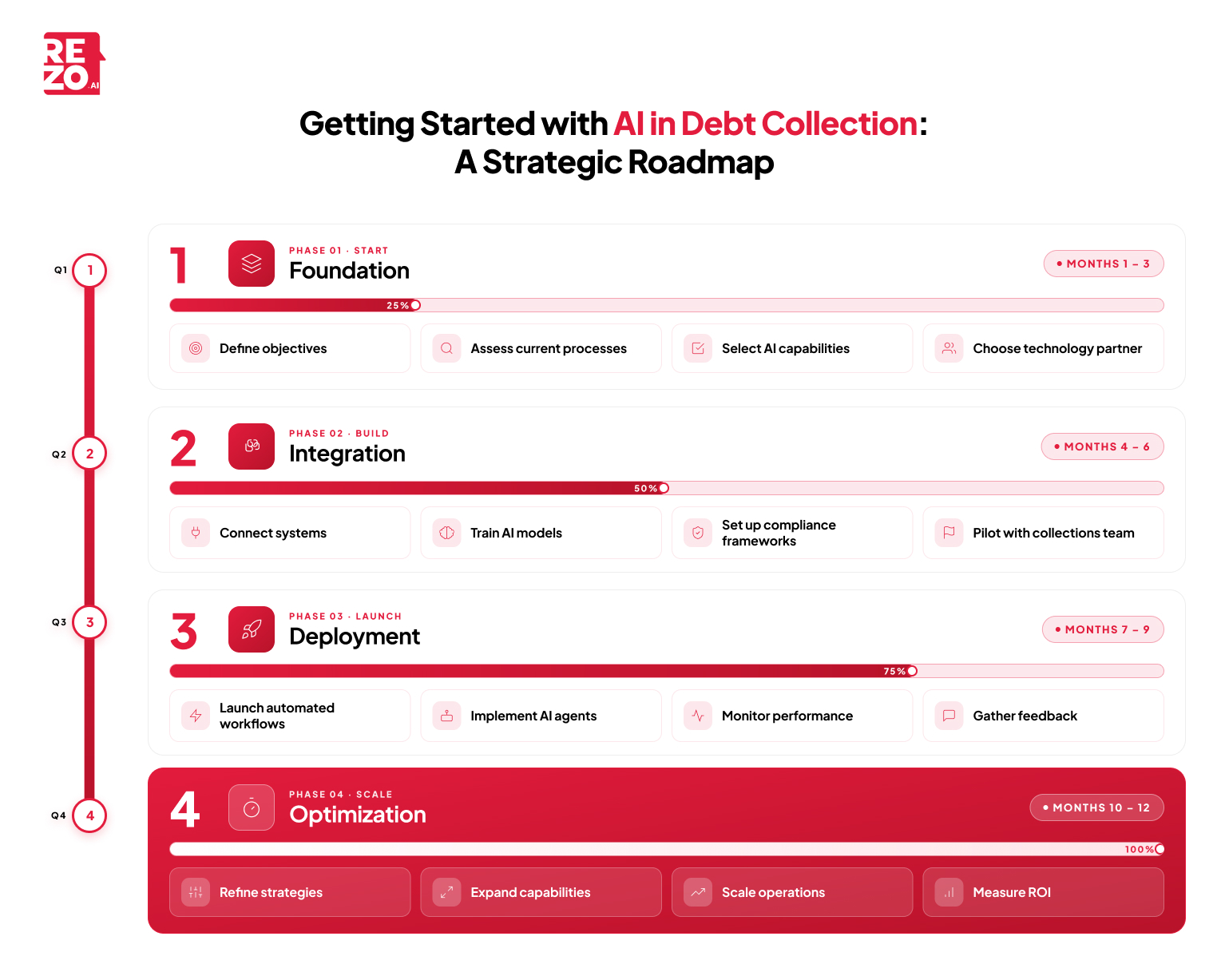

Getting Started: Implementing AI in Your Collection Strategy

If you are convinced that AI belongs in your debt collection strategy, where do you start with implementing AI solutions?

- Be clear about your objectives. Are you primarily focused on reducing operational costs, improving recovery rates, or enhancing customer experience through better collection strategies? While AI technologies can deliver all three, your initial focus will guide technology selection and implementation priorities for your collections teams.

- Understand that not all AI capabilities are created equal. Basic automation and rule-based systems are different from machine learning models and AI models, which are different from agentic AI systems that can make autonomous decisions within defined parameters. Your AI solution choice should match your organizational readiness and strategic needs for the debt recovery process.

- Consider how AI systems integrate seamlessly with your existing infrastructure. AI technologies need to connect with your existing collection management software, payment processing systems, payment portals, and customer data platforms. IBM’s recognition as a leader in the Forrester Wave for AI Decisioning Platforms highlights the importance of enterprise-grade platforms that can integrate across complex technology landscapes while maintaining data security.

- Do not underestimate regulatory compliance and ethical considerations in debt collection. The debt collection industry is highly regulated, and AI systems must operate within legal frameworks and collection laws like the Fair Debt Collection Practices Act while ensuring compliance with legal regulations. Algorithmic bias, data privacy, data security with advanced encryption protocols, multi factor authentication, and transparent decision-making are not just nice-to-haves, they are requirements for financial institutions implementing AI tools.

- Remember that AI in debt collection augments human agents and debt collectors rather than replacing them entirely. The most successful implementations use AI systems to automate processes, handle routine tasks, and provide behavioral insights, while experienced human agents and collections teams focus on complex cases, relationship management, and situations requiring empathy and human intervention.

The Future of AI-Powered Debt Collection

The trajectory for AI in debt collection is clear. Research by marketing firms conclude that the global market for AI solutions in debt collection is projected to grow from $3.34 billion in 2024 to $15.9 billion by 2034, representing a compound annual growth rate of nearly 17%.

This growth reflects not just adoption of current AI technologies and debt collection automation capabilities, but the emergence of new future trends. We are seeing early applications of hyper-personalization, where AI agent systems tailor every interaction based on comprehensive debtor profiles, payment behavior, and borrower behavior. Proactive default prevention is another frontier in debt collection strategies, where AI models identify high risk accounts likely to become delinquent and enable early intervention before accounts become outstanding debts.

Industry leaders are building debt collection capabilities directly into their CRM systems, making AI-powered collection processes accessible to financial institutions of all sizes. The barriers to entry for automated debt collection are falling as AI tools become more accessible.

As these advanced technologies mature, the question facing collection agencies and financial institutions is not whether to adopt artificial intelligence, but how quickly they can implement AI solutions effectively across their debt recovery process. Organizations that move decisively will gain competitive advantages in operational efficiency, recovery rates, and customer relationships through better engagement strategies and communication strategies. Those that delay risk falling behind in the debt collection industry where technology is rapidly becoming a differentiator.

Conclusion

Artificial intelligence is fundamentally transforming debt collection from a cost center focused on volume-based recovery to a strategic operation that balances financial outcomes with customer experience. The evidence from financial institutions is compelling: 40% reductions in operational costs, 10-25% improvements in recovery rates, and 30-35% boosts in customer satisfaction through better debt collection strategies.

For senior vice president level executives, CX leaders, and financial services decision-makers, the imperative is clear. AI technologies have moved beyond the experimental phase for debt collection. Real organizations are achieving real results with AI in debt collection. The question is no longer whether AI belongs in your collection strategy, but how quickly you can implement AI solutions across your debt recovery process while ensuring compliance with collection laws and maintaining a customer centric approach.

The future of debt collection is intelligent, efficient, and customer-centric, powered by AI agent systems, machine learning, predictive analytics, and sentiment analysis. Financial institutions and collection agencies that embrace this future now will be better positioned to navigate rising volumes of outstanding debts, tighter margins, and evolving consumer expectations through advanced debt collection automation. Those that wait will find themselves at a growing disadvantage as AI technologies transform the debt collection industry.

The transformation in debt recovery is happening. The only question is whether you will lead it or follow it.

Frequently Asked Questions

What is automated debt collection?

Automated debt collection is the process of managing and recovering outstanding payments with minimal human intervention. By using AI agents, tasks such as sending payment reminders, making reminder calls, and tracking customer accounts are automated.

What is an AI powered voice bot for debt collection?

AI voice bots are used to make payment reminder calls to customers. These agents can reach a substantially higher number of customers than human agents within the same timeframe.

How does Rezo AI help in debt collection?

At Rezo AI, our agentic AI voice bots have helped a leading NBFC achieve higher collection efficiency. You can read the full report here. Leading NBFC Achieved 10% Jump in Collection Efficiency with Agentic AI.

Frequently Asked Questions (FAQs)

Take the leap towards innovation with Rezo.ai

Get started now