From Loan Application to Asset Return: How Rezo AI Automates the Gold Loan Borrower Journey

From Loan Application to Asset Return: How Rezo AI Automates the Gold Loan Borrower Journey

Gold loans in India have always been a product built on trust. A family walks into a branch with an heirloom, hands it across a counter, and expects to walk out with cash and a clean promise that the ornaments will come back exactly as they were left. Gold loans are unusual in that way: most loans in this country are paperwork transactions, but gold loans are still, at heart, a physical handover between two people. That moment has not changed. What has changed is everything around it. Borrowers of gold loans want app-grade speed, branches are stretched thin, and the Reserve Bank of India has just rewritten the rulebook for the entire gold loan industry. This is where gold loan borrower journey automation moves from "nice to have" to a real operating model, and it is the gap Rezo AI is built to close for every lender writing gold loans at scale.

Why the Gold Loan Borrower Journey Needs a Rethink?

The gold loan market is sprinting. NBFC books of gold loans are projected to grow 30 to 35 percent in FY2026 on the back of strong gold prices, according to widely reported industry estimates. Demand for gold loans is being driven by households, micro-enterprises, and informal segments where other loans are simply not available. At the same time, the RBI's June and September 2025 Master Directions have collapsed thirty years of scattered circulars into one unified framework, and every lender writing gold loans has until April 1, 2026 to comply.

Tiered loan-to-value caps, borrower-present valuation, a seven-day asset return SLA after auctions, and per-borrower pledging limits are now non-negotiable for gold loans of any size. Regulatory consolidation across gold loans and broader Indian lending is forcing operating models to become more auditable and customer-centric in the same breath. The shape of gold loans as a product is changing, and the operating tempo around gold loans has to change with it.

That is the squeeze. The borrower of gold loans wants quicker, kinder, and more transparent. The regulator wants stricter, better-documented, and faster on the unwind for every set of gold loans on the book. A manual or semi-digital gold loan origination flow cannot keep both promises at the same time across millions of small loans. A unified, conversational journey can and it can do it without forcing the operations team to redesign how they handle loans on day one.

What Does the Modern Gold Loan Borrower Journey Look Like?

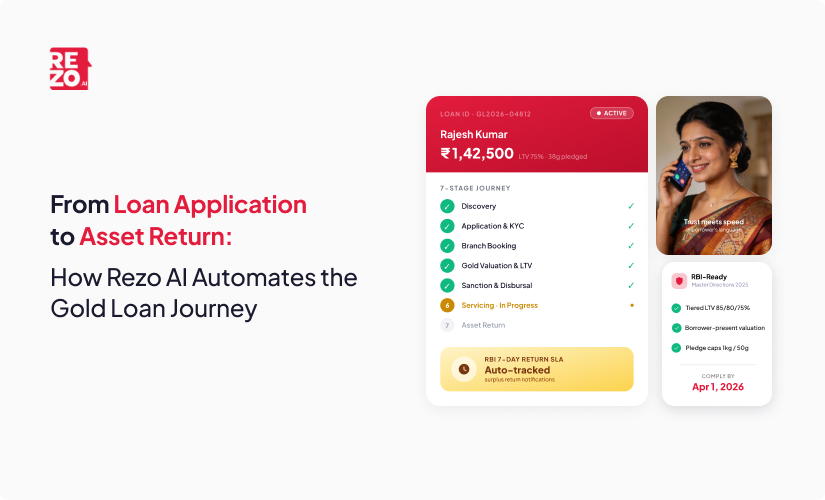

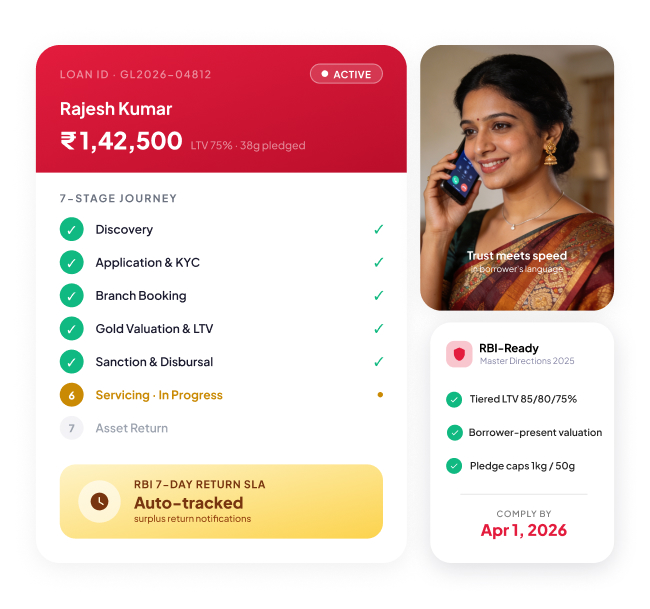

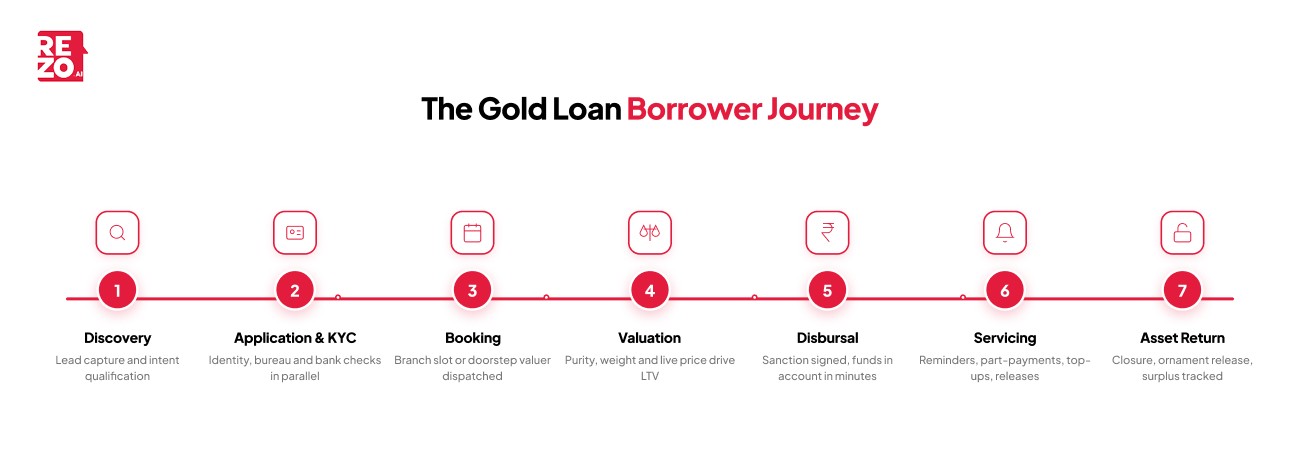

Before we talk about automation, it helps to name the canvas. A typical journey across gold loans moves through seven distinct stages of loan origination, and each one has its own moments of friction. The journey looks the same across small-ticket gold loans and high volume relationship gold loans handled by digital gold desks what changes is the cost of getting any single step wrong.

- Discovery: a borrower searches, sees an ad, gets a referral, or responds to a campaign for gold loans.

- Application and KYC: identity, address, and bank information are submitted, with document verification handled in line.

- Branch booking or doorstep valuation: the borrower picks a slot or a valuer is dispatched to begin the gold appraisal.

- Gold valuation and LTV computation: purity, weight, and live market price drive the loan amount.

- Sanction and disbursal: the offer is accepted and funds are credited.

- Servicing: interest reminders, part-payments, top-ups, and part-release of ornaments.

- Closure and asset return: full repayment, ornament release, and in some cases auction with surplus return.

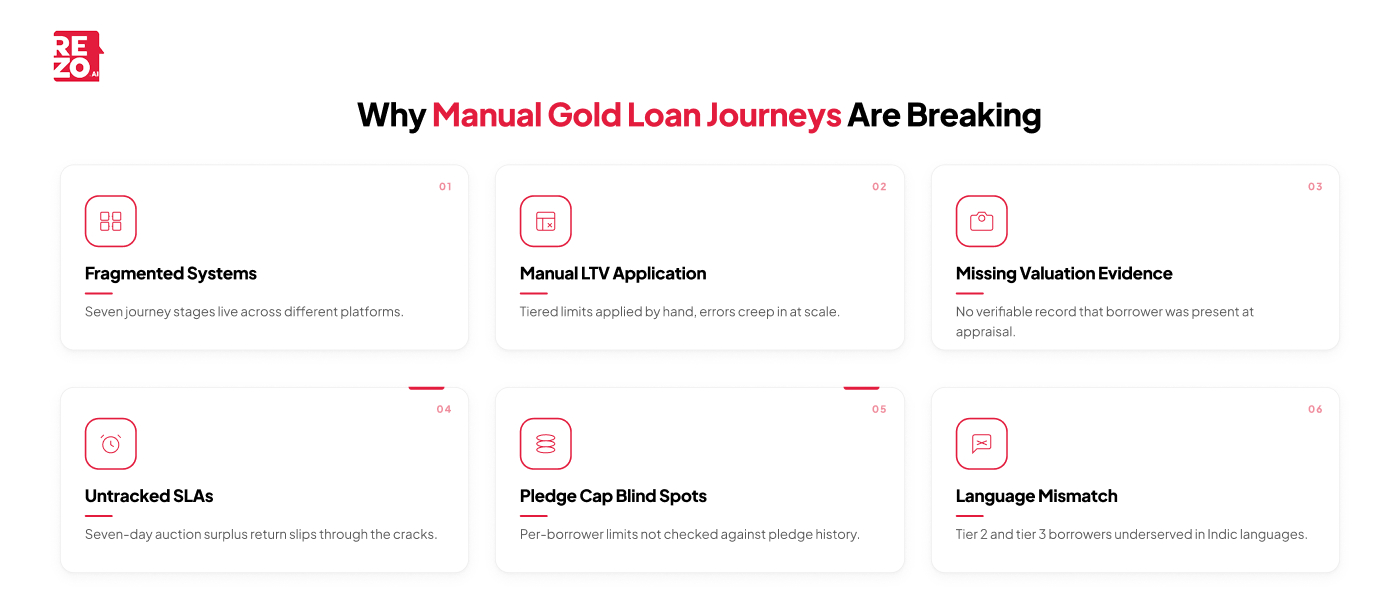

When all seven stages of the loan origination process live in different systems, on different teams, with different scripts and different SLAs, the borrower feels it. So does compliance. The cumulative result is that gold loans which should close in a single visit end up taking three, and gold loans which should be cleanly audit ready end up missing a document or two.

Why Manual Journeys Are Breaking Under the New Rules?

The new RBI framework is not just a tighter rulebook. It is a different operational tempo for the entire gold loan industry. Tiered LTV limits mean a ₹1 lakh loan against gold worth ₹1.2 lakh follows one rule, while a ₹6 lakh loan follows another. A spreadsheet-driven sanction process cannot apply the right ratio at scale across thousands of gold loans without manual errors creeping in, and the regulator now expects every batch of gold loans to be audit ready at any given moment.

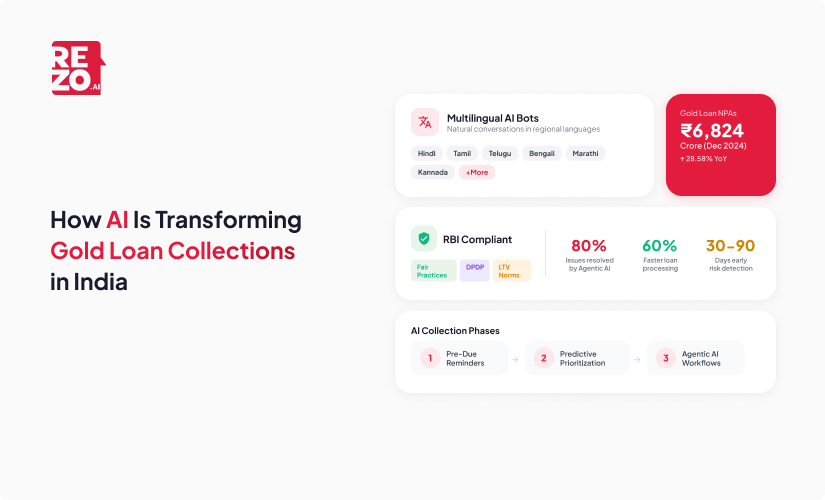

Borrower-present valuation introduces a brand-new evidence requirement for the gold valuation process. Every appraisal now needs a verifiable record that the borrower was actually there. The seven-day rule on returning auction surplus to the borrower is a customer service SLA that most NBFC gold loan operations teams were simply never built around. And the pledging caps of one kilogram of jewellery and fifty grams of coins per borrower must be checked across a borrower's history of gold collateral, not just the loan in front of you.

Layer on top of all that a multilingual borrower base spread across tier 2 and tier 3 India, with millions of small gold loans booked each quarter, and the math on a manual contact center is unforgiving. Deloitte's 2025 financial services outlook makes the same point about retail lending broadly: financial institutions that depend on linear, channel-siloed servicing are losing both efficiency and trust; and watching turnaround time, operational costs, and write-off ratios drift in the wrong direction across gold loans and other retail loans alike. The lenders that handle the highest volume of gold loans are the ones feeling this drift first.

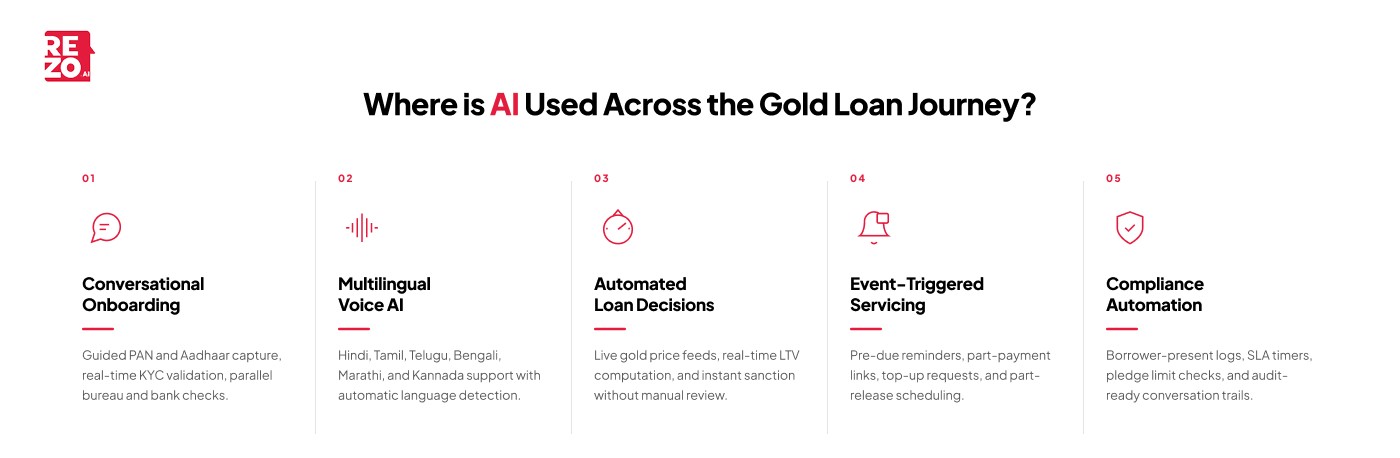

How Rezo AI Automates Each Stage of the Borrower Journey?

Rezo's AI Agent sits across voice, chat, WhatsApp, and email, which means it can act as one continuous thread through all seven stages of the gold loan origination system. Here is how that plays out in practice across modern gold loan operations like gold loan collections and digital gold workflows, and why a single platform changes the economics of gold loan lending at scale; particularly for lenders running tens of thousands of small gold loans every month, where audit trails and compliance requirements were previously the biggest source of slippage in the gold loan origination process.

Discovery.

Rezo's outbound voice and WhatsApp agents reach prospects in their preferred Indic language, qualify intent, and warm them to a branch visit or doorstep slot. The same conversation captures consent and feeds the lead straight into the LOS, kicking off loan origination cleanly and trimming customer acquisition cost.

Application and KYC.

A conversational application flow on chat or voice walks the borrower through PAN, Aadhaar, and contact details. Document images are captured in the same thread, and KYC automation drives real-time validation through biometric or OTP-based digital identity verification. Bureau, GSTN, and bank statement pulls happen quietly in the background, so the borrower experiences a single conversation instead of a form. This kind of digital onboarding turns loan applications from a multi-day chore into a guided exchange, with document verification, eligibility criteria, and bureau checks running in parallel rather than in sequence which is what makes the entire gold loan origination pipeline feel like a chat. The same loan applications flow handles top ups and renewal requests with the same lightweight conversational shape.

Branch booking and valuer dispatch.

The agent confirms a slot on WhatsApp, sends directions, and reminds the borrower a few hours before the appointment. For digital gold loan flows that include doorstep service, the AI assigns the nearest valuer and keeps the borrower informed every step of the way. For borrowers in tier 3 markets with limited access to physical branches, this doorstep model effectively brings the gold loan origination system to their living room.

Valuation moment.

Live gold prices flow into automated LTV calculations, and the agent explains the math to the borrower in their own language so there are no surprises later. Real-time eligibility checks and straight-through processing replace the spreadsheet approach that most legacy gold loan products still depend on, removing manual intervention from one of the most error-prone steps in loan processing for gold loans, while keeping every gold appraisal record audit ready.

Sanction and disbursal.

The sanction letter is delivered on WhatsApp or email instantly. Direct bank transfers enable faster disbursals straight to the borrower's account upon signing the digital agreement, and confirmations land across whichever channel the borrower uses most. If the borrower has questions about the loan decision, the same AI agent answers them with full context turning what used to be a multi-touch handoff into a single, transparent conversation. The platform's automated credit engine cross-references applicant data with bureau and bank records to support instant approvals and faster approvals on incoming gold loans, which is a meaningful shift for high volume gold lending desks and a direct lever on overall portfolio outcomes. Loan processing that used to take days now collapses into minutes, which is what gold loans need to compete with personal loans and other unsecured loans for share of wallet and a notable shift in recovery patterns across the gold lending book.

Servicing.

This is where most lenders quietly leak value across their gold loan products and other secured loans. Pre-due reminders, interest-only payment plans, part-release of ornaments, and top ups all run as event-triggered conversations. A borrower can ask, in 15+ Indian lanugages, what their outstanding is, request a part-payment link, or schedule top ups, without ever waiting in a queue. Self-service portals plug into the same conversational layer, so customers can track interest, view balances, and make repayments without a branch visit which lifts customer satisfaction across gold loans, smooths cash flow on the lender side, and reduces operational costs without adding load on the branch.

Asset return.

Closure is the moment of truth. Rezo orchestrates the appointment, confirms ID, and tracks the seven-day surplus return SLA on auctions with automated borrower notifications. The borrower walks out feeling that the lender kept its word, and the loan performance record closes cleanly with a full set of audit trails and audit ready evidence sitting behind it so when the regulator asks how a batch of gold loans was closed, the answer is already on file.

How Does Agentic AI Make Gold Loans Feel Human Again?

Automation has a reputation problem. Done badly, it feels like a wall between the borrower and the bank. Done well, it does the opposite it can deliver instant approvals on gold loans while keeping the relationship warm. That is why AI matters here, not as a cost-cutter but as a relationship tool that quietly raises the bar across all the loans a household might ever take.

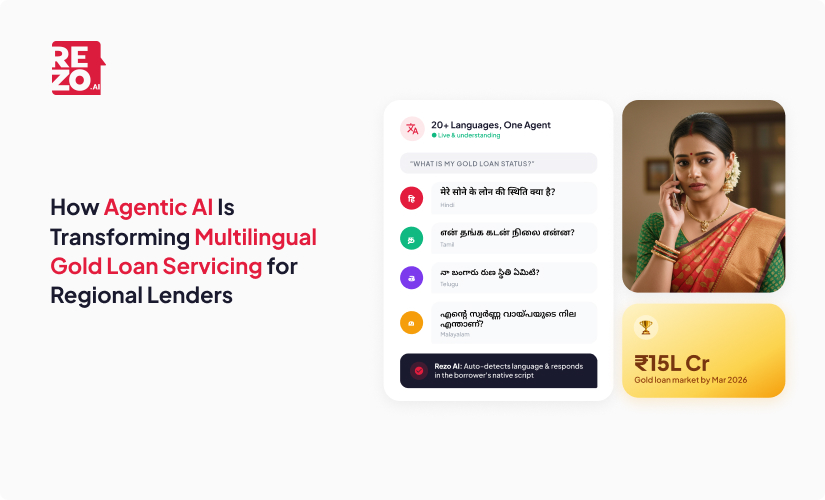

Rezo's voice AI handles Hindi, Tamil, Telugu, Bengali, Marathi, Kannada, and a long list of other Indian languages, detecting and switching automatically. Real-time sentiment analysis listens for distress, confusion, or anger, and quietly escalates to a human agent when the conversation calls for it. Context travels with the borrower, so a question started on WhatsApp can be picked up on a call without anyone having to repeat themselves. The result is a markedly better customer experience without adding headcount across the gold loans book and a noticeable shift in payment behaviour as borrowers feel kept in the loop, with borrower behaviour patterns feeding right back into the next conversation about future loans.

Therefore, the financial institutions that win retail credit are the ones that combine digital reach with human warmth at the moments that matter. For gold loans, those moments are valuation and asset return. Get them right, and the rest of the journey forgives itself.

How Does This Help Lenders Stay RBI-Compliant?

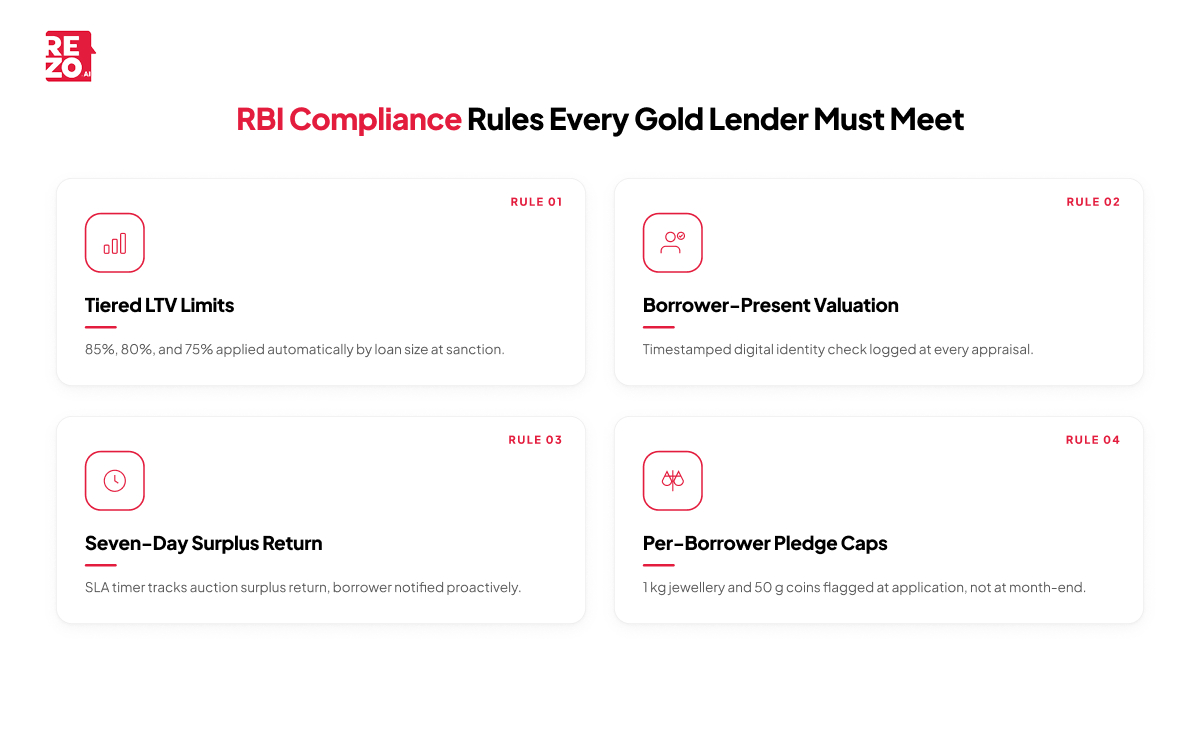

Compliance is no longer a quarterly audit problem. It is a per-transaction obligation, and gold loans now carry their own set of evidence requirements that did not exist a year ago. Agentic AI Agents bakes the new rules into the flow so they are not something the team has to remember. The platform keeps the gold loan business RBI compliant by default, with audit trails captured automatically as part of every conversation and every loan decision every gold loan that goes through the platform stays RBI compliant from sanction to closure, and every batch of gold loans is audit ready by default.

- Tiered LTV limits of 85, 80, and 75 percent are applied automatically at sanction, with the right tier picked from the loan amount.

- Borrower-present valuation is logged with a timestamp and a verifiable digital identity check.

- The seven-day surplus return rule is tracked via an SLA timer, with reminders to the operations team and proactive notifications to the borrower.

- Per-borrower pledge limits of one kilogram of jewellery and fifty grams of coins are flagged at the application stage, not at month-end reconciliation, so collateral management and audit trails stay clean across the entire book of gold loans.

The point is not that artificial intelligence replaces the compliance officer. The point is that compliance automation stops depending on whether someone remembered the rule on a busy Tuesday and that artificial intelligence quietly closes the gaps that human reviewers used to catch only after the fact. Audit-ready records sit alongside the conversation itself, which is how regulatory compliance for gold loans moves from a chase to a default and how a lender gets to complete compliance and clearer regulatory compliance coverage without slowing the front line. It is also how the operation stays ready for the next round of regulatory changes, because the rules live in the workflow, not in someone's memory, and decision making in loan origination stays consistent regardless of who is on shift.

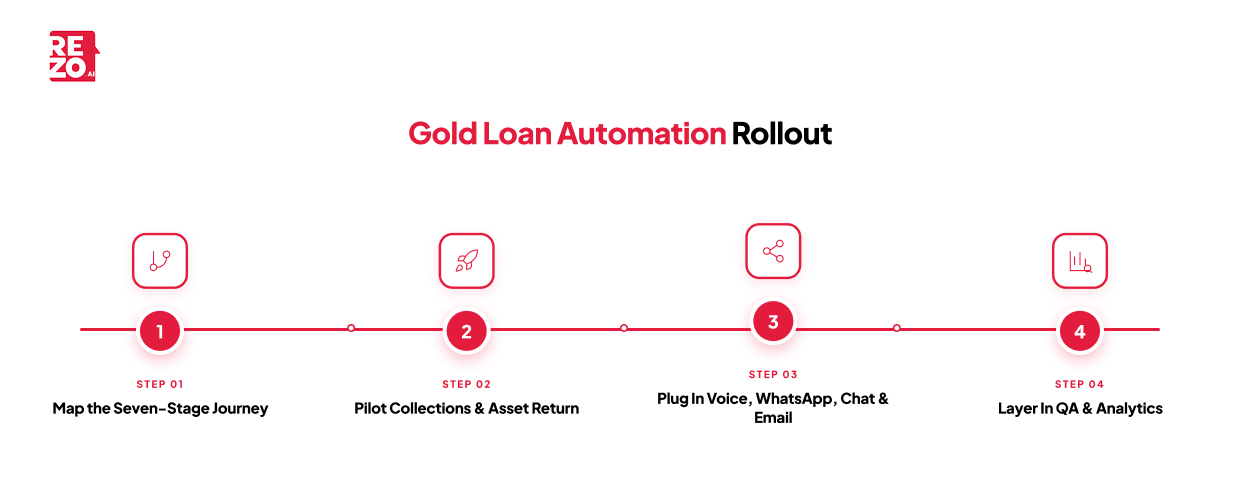

Implementation: How to Roll Out Gold Loan Journey Automation

Most lenders we work with are not starting from zero. They already have a gold loan origination system, a loan management system, a CRM, and some kind of contact center handling enquiries about gold loans every day. The right way to layer in journey automation is not a rip and replace. It is a careful, staged rollout that protects the existing gold loan origination system investments while folding in new AI technologies and AI tools on top, so the existing book of gold loans keeps performing while the new flow is built.

Step 1: Map the seven-stage journey across the systems you already have, starting with the gold loan origination system and how it hands off to servicing. Pinpoint where the borrower crosses a system boundary, because that is usually where friction lives and where manual processes still drag turnaround time and quietly inflate operational costs.

Step 2: Pick two or three stages with the highest pain or the biggest compliance risk and pilot there. Collections and asset return are usually the fastest to deliver visible wins on loan processing speed and to demonstrate how implementing AI changes the cost and speed of every loan that touches it.

Step 3: Plug Rezo into voice, WhatsApp, chat, and email so a single platform of agentic AI orchestrates conversations across channels. Borrowers should not feel a seam between channels, and the digital platform should hide the plumbing entirely.

Step 4: Layer in QA and analytics. Conversations are now a real time data source, not just a cost center. Use them to refine scripts, surface complaint trends, and pre-empt collection cases and to model borrower behaviour and payment behaviour so risk management sharpens with every cycle. The same conversation data also feeds machine learning models that score borrower profiles, predict default rates, and tighten loan approvals more reliably than static rules ever could. That is how ensuring transparency, decision making, and risk management start to reinforce each other.

The teams that approach this as a journey redesign rather than a contact center upgrade are the ones that see real movement in connect rates, collection efficiency, and complaint volumes across their gold loans book. Early adopters are also seeing operational efficiency gains that compound routine tasks shrink, manual processes fall away, and portfolio quality improves as gold loans get faster, better-documented, and more consistent. That is the digital transformation story playing out across the gold loan lending sector right now, and it is reshaping how financial institutions read market trends and adjust LTV limits in response across their portfolio of gold loans. For the leaders we work with, the key features that enable lenders to scale are not flashy they are clean data, audit ready trails, faster disbursals on gold loans, and a digital platform that the operations team actually trusts. The same approach raises operational efficiency in collections across other secured loans the lender writes.

The Borrower Journey Is the Product Now

Gold loans used to compete on interest rates and branch density. They now compete on how it feels to walk through the seven stages of loan origination. The lender that runs the cleanest journey from pledge to release, in the borrower's language, with the new RBI rules quietly built in, is the one that earns the next gold loan from that family and the one that builds a portfolio of gold loans and broader gold assets with stronger customer relationships at its core. The lenders that get this right will dominate gold loans in this cycle.

That is the promise of gold loan borrower journey automation. Across millions of gold loans every year, this is what good gold lending will look like for the rest of the decade.

Ready to see what your gold loan journey looks like with Rezo? Book a demo with us.

Frequently Asked Questions

Is income proof required to get a gold loan?

No. Most lenders, including major NBFCs, sanction gold loans based purely on the value and purity of the pledged ornaments. Standard KYC documents such as PAN, Aadhaar, and address proof are usually enough, with no salary slip, ITR, or CIBIL check required which is why eligibility criteria for gold loans remain among the most inclusive in the broader gold loan lending market.

Is the pledged gold safe with the lender?

Yes. Pledged ornaments are stored in insured, audited strongrooms with electronic surveillance and tamper-proof packets. The borrower receives a sealed pledge card, and the same ornaments must be returned in identical condition once the gold loan is fully repaid.

Can I repay a gold loan before the tenure ends?

Yes. Most lenders allow full or part prepayment of gold loans, and many waive foreclosure charges on floating-rate plans. Repayment options also include interest-only servicing with bullet principal repayment, or regular EMIs depending on the scheme chosen at sanction.

Frequently Asked Questions (FAQs)

Take the leap towards innovation with Rezo.ai

Get started now