Voice AI for Personal Loans: 4 Step Implementation Roadmap

Voice AI for Personal Loans: 4 Step Implementation Roadmap

Personal loan demand keeps climbing, but the people answering the phones have not multiplied. Borrowers want immediate answers in their language, at their hour, on their device, and they want a number on their EMI before they hang up. That gap, between what borrowers expect and what most lenders can staff, is where voice AI has quietly become the most consequential change in lending operations this decade.

This piece walks through what voice AI actually does across the personal loan lifecycle, its key capabilities, why it is finally working, and how serious lenders are putting it into production.

What Voice AI Really Does Across the Personal Loan Stack?

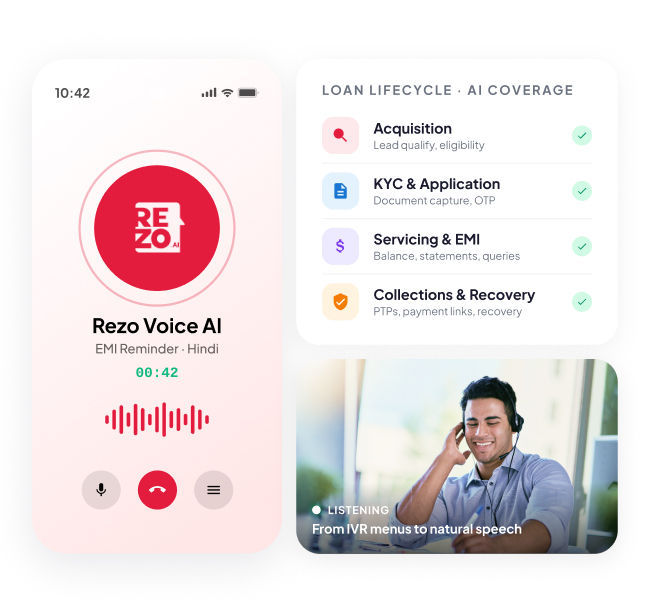

A voice AI agent for personal loans is a natural-language phone agent that talks, listens, and acts across the entire loan lifecycle, from the first inquiry to early stage nudges to the final EMI. It can qualify a borrower, walk them through eligibility, capture KYC details, send EMI payment reminders, manage repayment schedules, and negotiate a promise to pay, all in the borrower's preferred language. Many systems now layer in voice biometrics for identity verification, so authentication happens inside natural conversation rather than through a fragile OTP exchange.

It is not IVR with a friendlier voice. IVR is a rule tree. Voice AI is an intent-driven system built on natural language understanding that handles open-ended speech, holds context across turns, and reads and writes back into your LOS and servicing systems. It does not replace the underwriter or the recovery officer. It handles the conversation around them, so human agents get to spend their time on the complex cases that actually need a person. For a fuller view of how voice-first systems are reshaping the front office, our take on AI voice bots in banking covers the broader pattern.

Why Now? The Personal Loan Funnel Is Breaking, And Voice AI Is Fixing It

Three things have shifted at the same time. Volumes are up, expectations are up, and headcount cannot keep pace.

Gartner predicts conversational AI will reduce contact-centre labour costs by $80 billion by 2026, which tells you how seriously the analyst community is taking voice-first automation. McKinsey research shows organisations using generative AI in customer service see issue resolution per hour climb roughly 14%. PwC's analysis of banking puts voice AI efficiency gains in front-end and back-end operations as high as 35%.

Now layer in the Indian reality. NBFC books are projected to grow 15 to 17% annually through FY2028, and digital personal loan portfolios are headed past three lakh crore by FY2030. No collections head is hiring a 17% larger team every year. No customer service leader is letting AHT slip while call volume doubles. The maths only works if a meaningful share of conversations get handled by an AI agent that never sleeps, never drops empathy, and never strays from the script.

That is the gap voice AI now fills with production-grade reliability.

How Voice AI Works Across the Personal Loan Lifecycle?

The mistake most lenders make is treating voice AI as a single use case. The real value compounds when the same agentic layer runs across acquisition, application, servicing, and collections. Here is what that looks like in practice.

Acquisition and Lead Qualification

The first call a borrower makes is the most fragile moment in the funnel. A missed call is a lost lead, and a clumsy hand-off is almost as bad. AI voice agents pick up on the first ring, qualify intent, detect stress, ask the right disclosure-aware questions about income and existing obligations, give an indicative eligibility range, and book a callback if the borrower needs to think. On the outbound side, the agent works through warm leads at scale, using outbound calls to recover loan applications that stalled because the borrower got distracted halfway through the digital form. Industry research suggests AI voice agents can lift loan application completion rates by 15% or more by reaching out at the right moment with the right context.

KYC, Document Collection, and Application Completion

Once the borrower is qualified, voice AI walks them through KYC capture, OTP verification, and the document checklist. It does not replace digital uploads. It removes friction from them. When a borrower is on the phone confused about where to upload their salary slip, the agent guides them in real time and in plain language. AI agents can also initiate outbound calls, contact borrowers the moment a document requirement is flagged as missing, which keeps the file moving instead of waiting for the next manual calling attempt. Edge cases such as co-borrowers, irregular income, or non-standard employment trigger a warm transfer to a loan officer with full conversation context and borrower responses, so the loan officer picks up where the agent left off. Smarter systems even recognise returning callers and pull their borrower history immediately, so the conversation does not start from zero.

Servicing: EMI, Statements, and Account Queries

The vast majority of post-disbursal calls are repetitive. EMI date, outstanding balance, foreclosure quote, payment options, statement requests. Voice AI handles these loan inquiries end-to-end in seconds, not minutes, and delivers real-time application status without forcing the borrower into a portal or a callback queue. When a borrower wants to negotiate a tenure change or restructure, sentiment and complexity signals route the call to a human agent with the full account context already loaded, enhancing customer experience.

Collections and Recovery

This is where voice AI moves from nice-to-have to balance-sheet material. EMI payment reminders, soft-bucket nudges, promise-to-pay capture, and renegotiation conversations all run at scale across vernacular languages. A borrower in Coimbatore prefers Tamil. A borrower in Kolkata prefers Bangla. A borrower in Indore wants Hindi but with English loan terms. The agentic layer adapts, often detecting the borrower's preferred language from CRM records or the first few seconds of the call so the conversation never gets transferred just to switch tongue. Timely, personalised reminder calls also reduce missed payments, because borrowers get nudged before the due date passes rather than after. Every interaction is recorded, scripted to RBI fair-practices guidelines, and feeds into an audit trail your compliance team can defend. Our deep dive on AI in debt collection unpacks the recovery-side mechanics in more detail.

The Whys: What Personal Loan Teams Actually Get Out of Voice AI

Buyers do not buy features. They buy outcomes. When voice AI is wired correctly into the personal loan stack, the outcomes show up across four dimensions:

- Availability without staffing pressure: Every inbound call is answered, every outbound payment reminder goes out on time, and weekend volumes look like weekday volumes. Borrowers stop waiting on hold for routine loan inquiries.

- Multilingual reach: A Tier-2 or Tier-3 borrower from a genuinely multilingual borrower base talks in their language, which lifts right-party contact rates and trust on collections calls. Consistent multilingual support is what makes vernacular service feel like service, not a translation patch, enabling personalized borrower interactions.

- Consistent compliance: The disclosures, consent, and recording protocols happen on every call, not on the calls the QA team happened to sample. Sensitive data is captured and stored with the same controls every time.

- Cycle time compression: Pre-qualification in seconds, EMI follow ups at scale, and a faster handoff to human agents for the conversations that matter. Operational costs drop because manual calling shrinks to the cases where it adds real value.

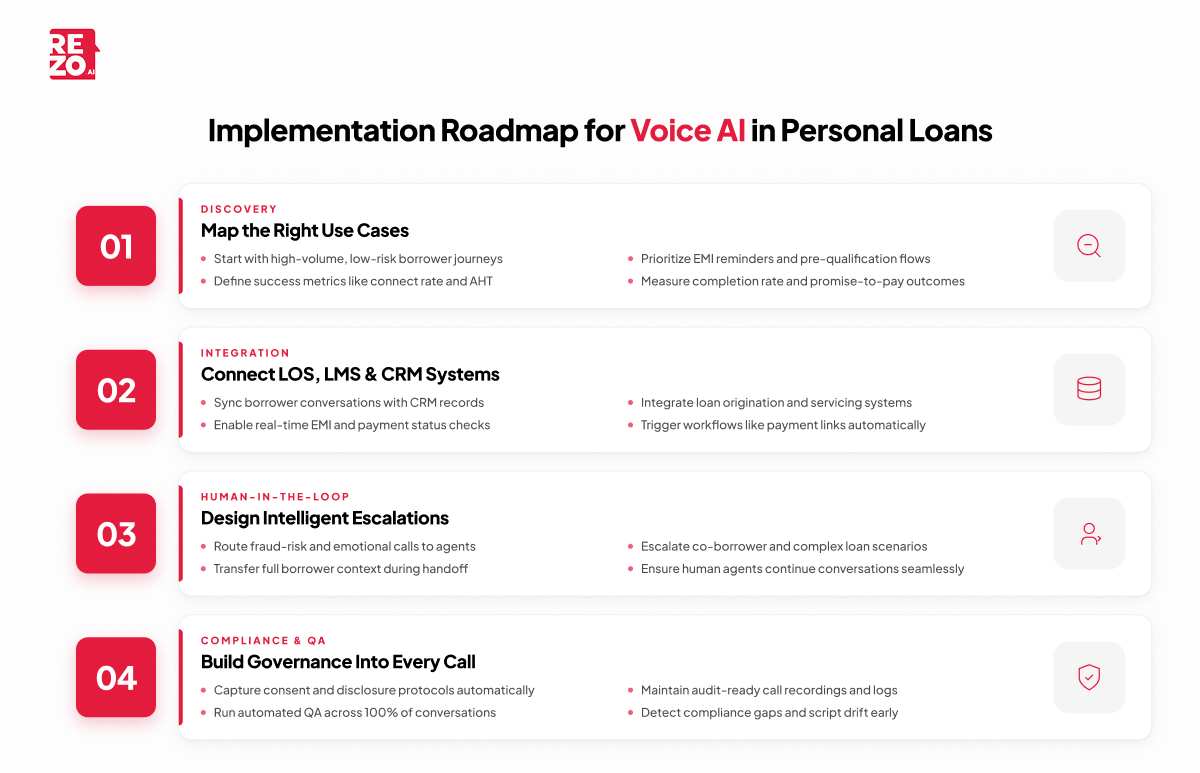

How to Implement Voice AI for Personal Loans?

The technology is the easy part. The implementation is where lenders separate themselves. Here is the pragmatic path that actually works.

Map the Use Cases Before You Buy the Tech

Pick one high-volume, low-risk journey to start. EMI payment reminders and pre-qualification are the usual entry points because they have clean data, repeatable scripts, and obvious success metrics. Define those metrics up front. Connect rate, average handle time, completion rate, promise-to-pay rate, and right-party contact rate. If you cannot measure it, you cannot improve it.

Integrate With Your LOS, LMS, and CRM

A voice agent is only as good as the data it can read and write. Two-way sync with the CRM means every call updates the borrower record with the latest borrower data. Live integration with the loan origination system means the agent can quote a real eligibility number for the loan amount the borrower asked about. A real-time feed from the loan management system means the agent knows whether the EMI was paid this morning before it starts the reminder call, and can trigger workflows like a payment link or a renegotiation flow without a human in the middle. Skip this integration work and you end up with a fancy phone bot that frustrates borrowers.

Design the Human-in-the-Loop

Voice AI should know when to step back. Escalation triggers worth defining upfront include fraud signals, high emotional sentiment, identity verification failures, multi-product comparison requests, co-borrower scenarios, and any conversation where the borrower explicitly asks for a human. When the human handoff happens, the agent transfers the full conversation context, not just the call. The human agent picks up informed, not cold. Our look at agentic AI voice agents walks through how this orchestration plays out in practice.

Build Compliance and QA Into the Pipeline

Lending is a regulated conversation. Consent capture, recording disclosure, and adherence to RBI fair-practices and TCPA-equivalent protocols are non-negotiable. Bake them into the script and the audit log. Then run automated QA on 100% of calls, not the 2% your manual QA team can sample. That is how you catch script drift early, and it is how you prove compliance when the regulator asks.

Voice AI Vs IVR: Why This Time It's Different

This question still comes up in every BFSI procurement deck, and the honest answer matters. Legacy IVR forces the caller into a rule tree the lender designed. It works when the caller knows exactly what they want and the tree was built thoughtfully. It breaks the moment the caller deviates. Pre recorded messages cannot adapt to a borrower whose question is one degree off-script.

Voice AI inverts the model. The caller speaks naturally, the agent figures out intent, and the conversation flows. Context carries across turns. Languages can switch mid-call. Edge cases hand off with full context. The result is the difference between a customer pressing "1" for the fifth time in frustration and a customer hanging up with their EMI question answered.

For a lender, the operational implication is simple. IVR caps your service quality at the rigidity of the tree. Voice AI lets quality scale with the sophistication of the model behind it.

What the Best Lenders Will Do Differently in the Next 18 Months?

The lenders pulling ahead are doing three things the rest are not.

First, they are treating voice AI as an operating layer, not a channel. The same agentic intelligence that runs the inbound voice calls also runs the WhatsApp follow-up, the chat conversation, and the email reminder. Borrower experience stays continuous across surfaces, and the lender stops paying for four disconnected stacks. Our comprehensive guide to AI in banking goes deeper on this shift.

Second, they are treating the voice agent like a teammate. They review its performance, coach it with feedback, push QA findings back into the prompt, and measure it on business outcomes such as roll-rate, NPS, and book growth, not just on call metrics.

Third, they are choosing platforms built for enterprise BFSI workloads. That means voice-first agentic AI with vernacular coverage, deep CRM and LOS integration, and the compliance scaffolding that lending demands. Rezo.ai already powers voice-first conversations at this scale across leading Indian financial institutions, handling millions of voice calls a day with the connect rates and compliance posture enterprise BFSI requires.

Conclusion

Voice AI is no longer a pilot inside personal loans. It is becoming the spine of the loan journey across acquisition, servicing, and collections. The lenders that wire it end-to-end will compress cost, lift speed, and improve borrower experience at the same time, which is rare in this industry. The ones that wait will pay for it twice, once in lost loans and again in oversized service teams.

Frequently Asked Questions

Can a voice AI agent approve a personal loan on its own?

No. Voice AI agents handle qualification, document capture, and the borrower conversation, but the credit decision and loan processing apporval still sits with the lender's underwriting engine and risk policy. The agent's job is to accelerate the intake, capture clean borrower data, and route eligible borrowers cleanly.

Is voice AI safe and compliant for personal loan calls in India?

Yes, when configured for it. A compliant deployment captures consent on every call, follows RBI fair-practices guidelines, records and stores audio with secure handling of sensitive data, and produces a full audit trail. The platform you choose has to be built for that out of the box.

How is voice AI different from a chatbot for personal loans?

A chatbot handles text on a screen. Voice AI handles a phone call in natural spoken language, with tone, sentiment, and multilingual switching. For borrowers who prefer to talk, especially in Tier-2 and Tier-3 markets, voice AI reaches a much wider audience than chat alone.

Frequently Asked Questions (FAQs)

Take the leap towards innovation with Rezo.ai

Get started now