Agentic AI-Powered Dispute Resolution for Card and Transaction Complaints in Banks

Agentic AI-Powered Dispute Resolution for Card and Transaction Complaints in Banks

When a customer disputes a transaction, every hour counts. For operations leaders in financial services managing hundreds of thousands of monthly interactions, the pressure to resolve card and transaction complaints quickly has never been greater. Agentic AI-powered dispute resolution is emerging as the definitive solution to this challenge. With dispute volumes climbing and customer expectations rising, financial institutions must rethink how they handle these critical moments of truth.

The stakes are clear: 62% of consumers say their trust in a financial institution is more influenced by how disputes are handled than the fraud event itself. For organizations still relying on manual tasks that stretch resolution times to 120 days, the risk of customer attrition is real and growing.

The Growing Challenge of Card and Transaction Disputes

The scale of the dispute problem in financial services is staggering. Between 50 million and 100 million disputes occur annually in the United States alone. Last year, Americans disputed a remarkable $83 billion in charges, according to Salesforce research. This volume creates operational strain that traditional dispute workflows simply cannot absorb efficiently.

The financial burden is equally significant. McKinsey reports that the top 15 US institutions spend approximately $3 billion annually on chargeback management and dispute handling. Making matters worse, chargeback process costs have increased 16% compared to 2022, a trend that threatens operational sustainability and contributes to revenue leakage.

Resolution timelines compound these challenges. While the industry best practice targets 30-day resolution, many financial services organizations still take excessive time:- up to 120 days, to close complex cases. This extended timeline damages customer relationships at a critical moment. According to industry research, 62% of consumers indicate that their trust in a financial institution is shaped more by the dispute experience than by the original fraud incident.

For operations leaders overseeing large contact center operations, these numbers represent both a problem and an opportunity. The opportunity lies in transforming dispute management from a cost center into a customer experience differentiator.

What Is Agentic AI in Dispute Management?

Agentic AI represents a fundamental evolution beyond traditional rule-based automation. Where conventional systems follow predetermined scripts and decision trees, agentic systems operate autonomously, capable of perceiving context, reasoning through complex scenarios, planning multi-step actions, and executing decisions independently.

In the context of dispute management, this means AI agents that don’t simply route cases or auto-populate forms. Instead, agentic systems analyze transaction patterns, retrieve relevant evidence, apply card network rules, and determine appropriate resolutions while learning from each outcome to improve future performance.

The distinction matters for leaders evaluating technology investments. Rule-based automation handles predictable, repetitive tasks efficiently. Agentic AI handles variability, ambiguity, and complex disputes, the defining characteristics of chargeback management.

Adoption is accelerating across the industry. McKinsey's research indicates that 85% of institutions already deploy some form of AI. This adoption rate reflects growing confidence in the technology’s ability to deliver results while maintaining the governance standards that financial services requires.

How Agentic AI Transforms the Dispute Lifecycle?

Agentic systems impact every stage of the dispute journey through intelligent workflows. During intake and classification, AI agents categorize incoming disputes across all channels, distinguishing between fraud-related claims and service-related complaints that require different resolution paths.

In the investigation phase, the AI autonomously retrieves transaction data, merchant details, cardholder history, and relevant documentation. This evidence gathering, which traditionally required hours of manual data entry and repetitive tasks, happens in seconds through real-time data handling.

For decision-making, AI agents apply card network rules from various payment processing networks alongside regulatory compliance requirements and patterns learned from historical outcomes. The systems weigh multiple factors simultaneously to determine the appropriate resolution, reducing human errors common in manual reviews.

Finally, throughout resolution and customer communication, the AI maintains proactive contact with status updates, reducing the anxiety that often accompanies disputed transactions.

What are the key applications in Card and Transaction Disputes?

The practical applications of agentic AI span the full range of card and transaction disputes that operations teams encounter daily.

For unauthorized transaction claims, AI agents detect patterns in cardholder behavior, verify whether transactions align with established spending profiles, and accelerate resolution by compiling evidence automatically. When the data clearly supports the customer’s claim, faster resolution can happen within hours rather than weeks.

Merchant dispute automation represents another high-value application. Financial institutions using AI-powered solutions can automate evidence compilation for chargeback representment, significantly improving win rates.

Friendly fraud detection, where customers dispute legitimate transactions, poses particular challenges for manual reviews. AI agents distinguish between legitimate disputes and first-party fraud attempts by analyzing transaction context, customer history, and behavioral patterns that human reviewers might miss, delivering actionable insights in real time.

Multi-channel intake unification solves another common pain point. When disputes arrive through phone calls, emails, mobile apps, web portals, and branch visits, dispute automation consolidates these inputs into unified case files, providing a unified view that prevents duplicate efforts and ensures consistent handling regardless of entry point.

What are the Real-Time Payment Dispute Challenges?

The rise of instant payments creates dispute scenarios where traditional timelines simply don’t apply. When funds move in seconds, customers expect faster dispute resolution to match that pace.

Agentic systems enable immediate fraud detection and dispute initiation for real-time payment transactions. TCS research highlights how AI solutions can monitor transactions as they occur, flagging suspicious activity and initiating protective measures before funds become irrecoverable. This real-time capability is essential as instant payment adoption continues to grow.

Human-AI Collaboration in High-Stakes Decisions

The most effective implementations of agentic AI in customer service embrace collaboration rather than complete automation. AI agents handle routine cases autonomously, delivering what Genpact estimates as a 50% reduction in operational time spent on case reviews.

Human agents then focus their expertise on complex cases that require nuanced judgment. Escalation protocols ensure that disputes involving unusual circumstances, high dollar amounts, or regulatory sensitivities receive appropriate human intervention and oversight.

This balanced approach also addresses customer expectations. According to Industry Research, 74% of consumers say that transparency in fraud investigations builds trust. When human agents remain involved in appropriate cases, customers feel their concerns receive genuine attention.

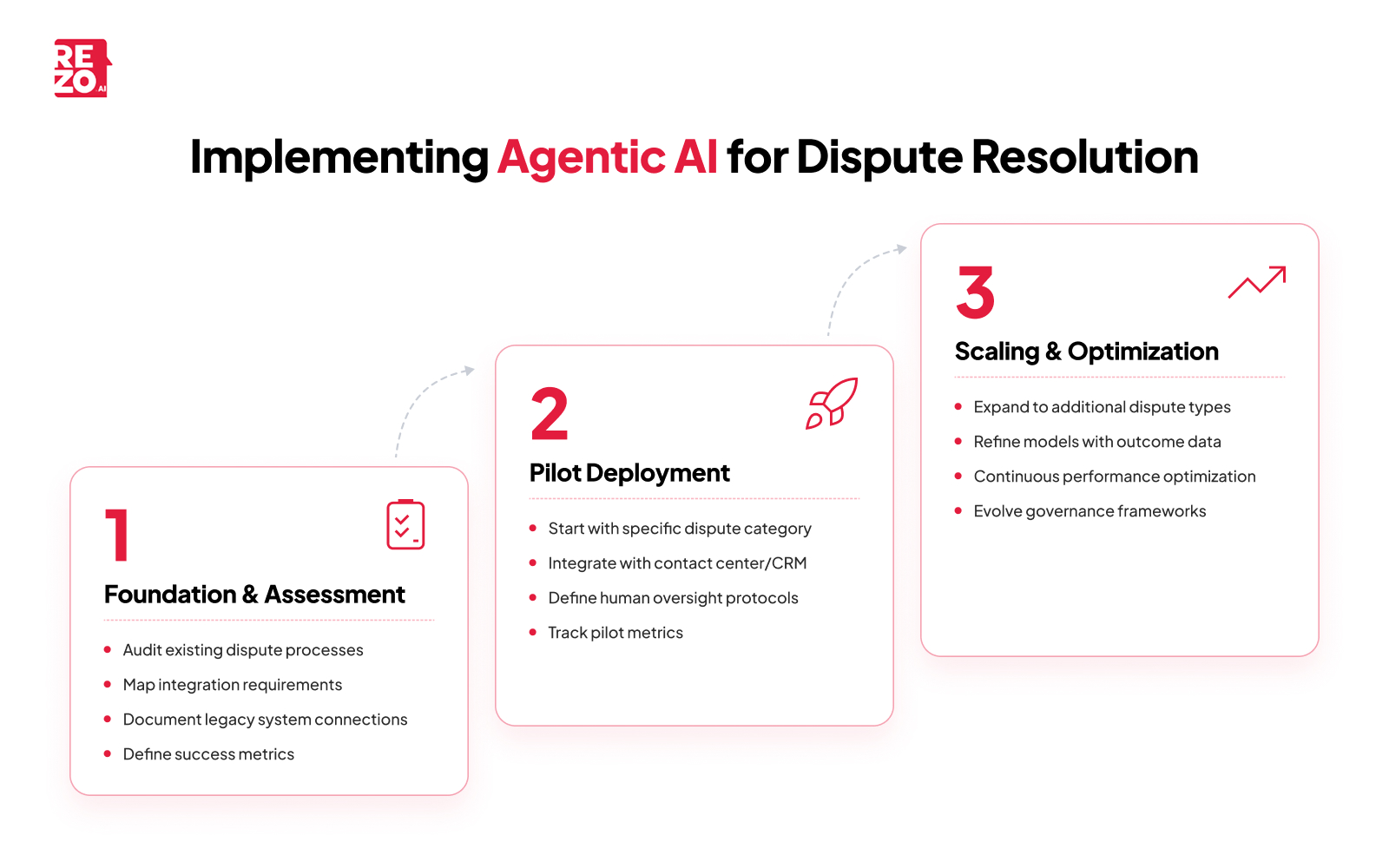

How to Implement Agentic AI for Dispute Resolution?

Successful implementation requires a phased approach that accounts for both technical complexity and organizational change management. Data says 75% of financial services organizations struggle to implement new payment solutions due to outdated infrastructure. Recognizing this reality, effective implementation plans break the journey into manageable stages.

Additionally, 88% of financial services leaders agree that organizations need to innovate faster, according to joint Forrester and AWS research. This urgency must be balanced with careful execution to achieve lasting results.

Phase 1: Foundation and Assessment

The first phase focuses on understanding current state and preparing for transformation. Operations teams should audit existing dispute workflows to identify specific pain points, bottlenecks, and automation opportunities.

Mapping system integration requirements proves essential during this phase. Connections with core systems, card processing platforms, payment gateways, and customer communication channels must be documented. Legacy system modernization can decrease errors by 40%, making infrastructure assessment a critical early step.

Success metrics should extend beyond operational costs savings to include resolution time, customer satisfaction scores, regulatory compliance adherence rates, and resource allocation improvements. Establishing clear performance metrics early enables meaningful progress tracking.

Phase 2: Pilot Deployment

The pilot phase limits scope intentionally to enable learning and refinement. Starting with a specific dispute type:- such as low-value chargeback disputes allows teams to validate AI performance before broader deployment.

Integration with existing contact center tools and CRM platforms ensures that AI capabilities enhance rather than disrupt established workflows. Human oversight protocols and escalation triggers require careful definition during this phase, establishing the boundaries within which AI agents operate autonomously.

Pilot metrics should track both operational outcomes and customer experience indicators to build the business case for expansion.

Phase 3: Scaling and Optimization

Based on pilot learnings, the AI deployment expands to handle more disputes and additional dispute types. Machine learning models refine their decision-making using outcome data from initial deployments, improving accuracy over time.

McKinsey research indicates that next-generation operating models can achieve 30% or greater efficiency gains. Perhaps more importantly, customer-impacting errors can be reduced by 80% with AI-driven solutions, according to the same research. These outcomes typically emerge as implementations mature through continuous optimization.

Governance, Compliance, and Risk Considerations

Leaders in financial services rightly prioritize governance when evaluating AI implementations. Dispute resolution touches regulatory requirements, card network rules, and consumer protection standards that demand rigorous compliance.

Alignment with card network rules must be built into AI decision frameworks from the outset. Card issuers must ensure their systems can adapt to updated requirements without extensive reconfiguration as these rules evolve.

Consumer protection requirements vary by jurisdiction and transaction type. AI tools must apply appropriate rules based on transaction characteristics while maintaining audit trails that demonstrate regulatory compliance to regulators upon request.

Governance frameworks for agentic AI emphasize the importance of explanations. When regulators or customers ask why a particular decision was made, organizations must be able to provide clear, documented reasoning. This transparency requirement shapes how machine learning models are designed and deployed.

Data governance extends these considerations to the information AI systems access and generate. Protecting customer data while enabling AI effectiveness requires careful architecture, proper data handling protocols, and ongoing monitoring.

The Future of Dispute Resolution with Agentic Commerce

Looking ahead, the dispute landscape will grow more complex before it simplifies. Agentic commerce, where AI agents make purchases on behalf of consumers, is emerging as a significant trend. This shift will create entirely new categories of disputes requiring new solutions.

Datos Insights projects that chargebacks volume will climb 24% from 2025 to 2028, reaching 324 million chargebacks globally. Some portion of this growth will stem from new dispute types including bot authentication failures, AI-to-AI transaction errors, and liability questions when autonomous agents act beyond their authority. Understanding emerging dispute trends will be essential for business planning.

Financial institutions must prepare not only for AI-resolved disputes but also for AI agent-initiated disputes. The same technology powering dispute automation will eventually power dispute initiation on the customer side.

Consumer sentiment supports continued AI adoption in fraud-related use cases. According to Salesforce research, 77% of consumers show interest in AI-powered fraud detection and prevention. This receptiveness provides a foundation for deeper AI integration in dispute responses and communication.

Getting Started with AI-Powered Dispute Management

For operations leaders ready to act, the path forward begins with honest assessment. Conducting a dispute audit reveals specific automation opportunities and system integration requirements unique to each institution. Understanding your business needs helps prioritize which solutions to evaluate first.

Evaluating technology partners should prioritize proven integrations and demonstrated compliance capabilities. The vendor landscape includes tools ranging from point solutions to comprehensive chargeback management platforms.

Throughout implementation planning, customer experience must remain central alongside operational efficiency goals. The most successful implementations deliver both cost savings and improved customer satisfaction, addressing both business needs and customer expectations.

Building internal capabilities for AI governance and oversight ensures sustainable results. Teams need skills to monitor AI performance, analyze reason codes, refine decision criteria, and maintain compliance as regulations evolve.

The opportunity to transform dispute management from operational burden to competitive advantage is real and achievable. Financial services organizations that move decisively will establish positions of strength as dispute volumes continue to grow achieving faster resolution while reducing operational costs.

Frequently Asked Questions

How long does AI-powered dispute resolution take compared to manual processes?

AI-powered dispute resolution can complete straightforward cases in hours rather than weeks. While manual tasks often stretch resolution to excessive time periods of up to 120 days, AI solutions achieve the industry benchmark of 30 days or less by automating evidence gathering, pattern analysis, and decision documentation simultaneously, eliminating lost revenue from prolonged chargebacks.

What KPIs should banks track for AI dispute resolution success?

Beyond cost savings, banks should measure average resolution time, first-contact resolution rates, chargeback win rates, customer satisfaction scores (CSAT), compliance adherence rates, escalation frequency to human agents, and reduction in customer-impacting errors.

Frequently Asked Questions (FAQs)

Take the leap towards innovation with Rezo.ai

Get started now