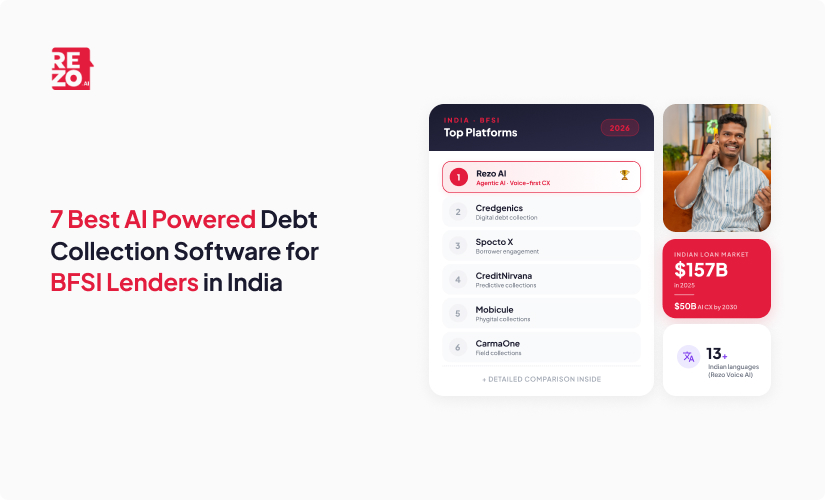

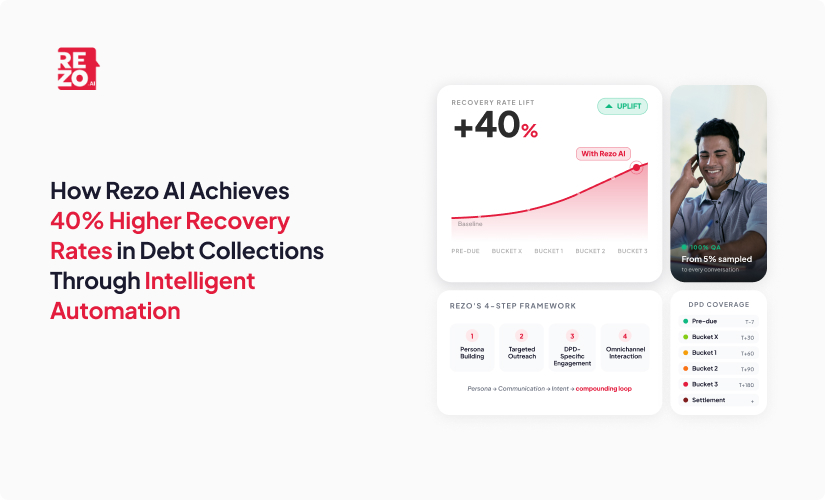

How Rezo AI Achieves 40% Higher Recovery Rates in Debt Collections Through Intelligent Automation

How Rezo AI Achieves 40% Higher Recovery Rates in Debt Collections Through Intelligent Automation

Debt collection teams across BFSI are running the same play they ran a decade ago, just with more agents on the floor. The result is predictable. Connect rates plateau, costs creep up, debt recovery curves flatten, and bad debts keep slipping into the next quarter. This blog walks through how at Rezo AI we have achieved 40% higher recovery rates in debt collections for leading NBFCs, through intelligent automation, why human-led collection strategies are stuck, and how the right four-step framework built around AI in debt collection rather than around the dialer; turns the recovery process into a system rather than a sprint. The shift matters because the debt collection industry is no longer competing on headcount; it is competing on artificial intelligence, debt collection automation, and how quickly collection efforts can be tuned cohort by cohort.

Why Human-Led Debt Collections Is Hitting a Ceiling

Recovery teams are not under-skilled. They are under-orchestrated. Gartner benchmarks show that a typical call center agent inside a manual debt collection process handles around 70 phone calls a day, while only about 5 percent of those calls go through quality checks. That is a debt recovery model that depends on volume, attention, and luck, often all at the same time. Inside large debt collection agencies, the math gets worse the more phone calls per agent, the lower the share of conversations that any quality lead can actually inspect.

Four limitations keep showing up when we audit a human-led debt collection operation:

- Resource-intensive processes. Manual paperwork, repeated phone calls, and field visits stretch response times and inflate operational costs per recovered rupee, weighing heavily on the broader recovery process and on the debt recovery process for every cohort downstream.

- Organizational data fragmentation. Bounce history, persona signals, and payment behavior sit in three different systems, so outreach is reactive instead of pattern-driven, leaving collections teams without a single view of customer behavior or customer interactions across channels.

- Communication quality issues. Tone drift across thousands of collection calls a day leads to compliance risk and reputational damage. You cannot manage what you only sample at 5 percent, and you certainly cannot enforce fair debt collection practices that way.

- Limited performance insight. Without conversation-level data analytics, you optimize what you can count, not what actually moves recovery rates. Collection strategies in this state remain anecdotal rather than evidence-led.

These are not motivation problems. They are coordination problems. Once you accept that, the path to a 40 percent uplift in recovery rates becomes a design exercise rather than a staffing exercise, and the debt collection industry begins to look very different from the one most BFSI leaders inherited. The winners in modern debt collection will not be the largest collection agencies; they will be the most data-fluent ones.

What Intelligent Automation Actually Changes in Debt Collections

Intelligent automation in debt collection is not a chatbot bolted onto a dialer. It is a layer of artificial intelligence agents that decide who to contact, when to contact them, on which channel, with what script, and then learn from every customer interaction. The lift comes from that decision layer, not the channel itself. Artificial intelligence reframes debt collection as a continuously learning loop, where every conversation makes the next debt collection attempt smarter and where collection strategies adapt at the cohort level instead of the campaign level.

McKinsey reports that lenders going digital-first see multi-point lifts in resolution rates and a 15 percent drop in collection costs. One European bank automated 90 percent of customer communication using machine-learning models that draw on around 800 variables, achieving more than 30 percent savings with no operational dip. Gartner forecasts that agentic AI will autonomously resolve 80 percent of common customer service issues by 2029, cutting operational cost by 30 percent. The shift is moving faster than most CX leaders expect: over 70 percent of financial institutions are projected to use AI at scale by late 2025, up from just 30 percent in 2023, and the global market for AI in debt collection is forecast to grow from $3.34 billion in 2024 to $15.9 billion by 2034: a near-17 percent CAGR that reflects how quickly debt collection automation has moved from pilot to default. Put differently, AI in debt collection is no longer a competitive edge for early adopters; it is becoming table stakes for any lender that wants to keep cash flow healthy and bad debts contained.

Rezo's Platform brings two capability layers together. On one side, AI agents automate borrower engagement across voice, chat, email, and WhatsApp, handling outreach in 10+ vernacular languages with hyper-personalized scripts tuned to each borrower's persona and bucket: the kind of personalized communication and personalized customer interactions that static phone calls and templated reminders have never been able to deliver at scale. On the other side, AI agents analyse every conversation, surfacing intent, sentiment, risk signals, and behavioural patterns from interaction data. Predictive analytics applies statistical methods and machine learning to historical data, flagging delinquent customers likely to miss the next instalment before late payments and a missed instalment harden into a bad debt. The combined effect across BFSI deployments is a measurable lift in connect rates, a meaningful drop in cost per recovered account, a healthier customer experience, and stronger recovery curves across both pre-due and post-due buckets; especially in vernacular-heavy Tier-2 and Tier-3 markets where traditional debt collection has historically struggled to scale.

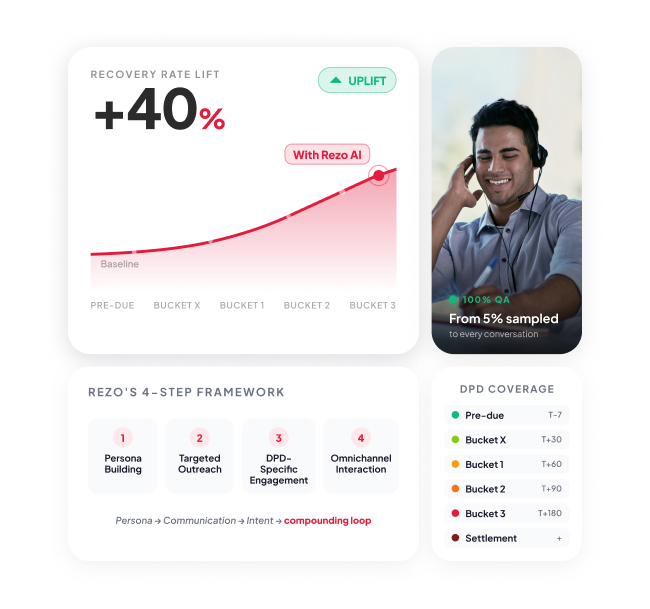

How Rezo's 4-Step Framework Lifts Recovery Rate

Rezo's framework is the spine of the recovery uplift. It is built to be digital-first and data-driven at every stage, blending first-party customer data with Rezo's data lake to power debt collection strategies that flex by persona, bucket, and channel.

- Profile-Based Persona Building. Every borrower is profiled using payment history, loan attributes, and behavioural signals from historical data before the first call goes out, so collection strategies are shaped by evidence rather than instinct.

- Targeted Communication Strategy. Outreach is prioritized by loan details and persona fit, not by the order accounts appear in a list, so collection efforts concentrate on the highest-yield delinquent accounts first.

- DPD-Specific Engagement Strategy. Mass-outreach signals feed back into the engine to refine the debt collection process at every bucket, so each new attempt is informed by the last.

- Omnichannel Interaction. Scripts are tuned per bucket and rendered across voice, chat, email, and WhatsApp, with intent and dialect handling in 15+ Indian languages for deeper Tier-2 and Tier-3 penetration. Automated reminders go out through each borrower's preferred channel, so thousands of customized messages can be delivered without the dialer-led monotony of legacy collection efforts.

The reason this framework lifts recovery is not any single step. It is the loop. Persona shapes communication. Communication generates intent signals. Intent signals refine the next debt collection attempt. By the time a borrower is in Bucket 1, the system already knows their preferred channel, time-of-day, and language, and so the connect rate compounds. This is what well-designed collection agent actually delivers not a faster dialer, but a smarter debt collection process that gets better with every interaction. You can see this design pattern at work in Rezo's broader thinking on AI in debt collection.

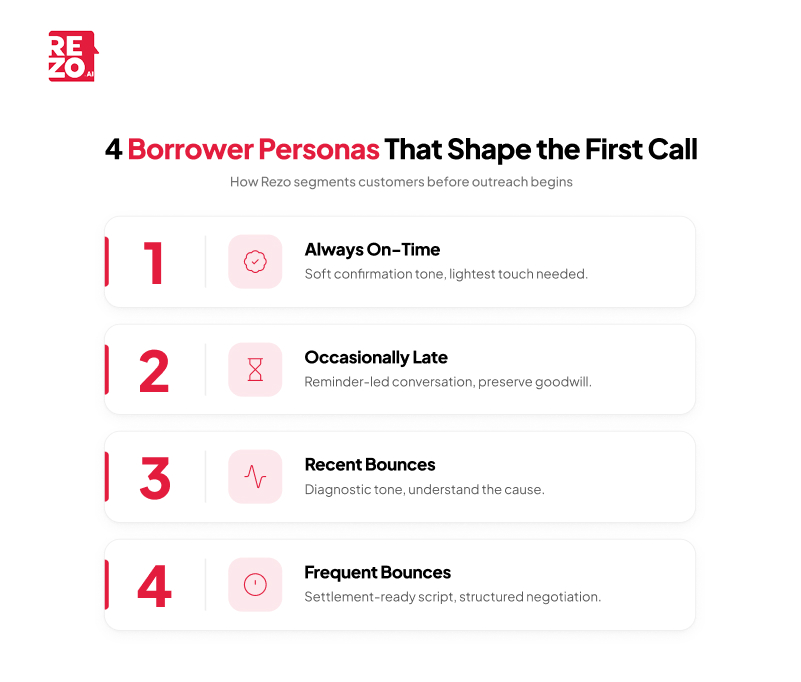

How Persona Building Sharpens the First Conversation

Behavioural personas in Rezo's model fall into four practical buckets defined by customer behavior: always on-time, occasionally late, recent bounces, and frequent bounces. Each persona is enriched with bounce count, payment history, and the customer's CRIF score, which clients provide as part of onboarding. Analyzing historical data this way produces precise DPD bucket identification at the start of every campaign, so the right tone hits on the first attempt rather than the third.

This is the difference between calling a "recent bounce, always on-time" customer with a soft reminder versus dialing a "frequent bounce" account with a settlement-ready conversation. Same DPD, very different conversation, very different recovery curve. The result is personalized communication that meaningfully lifts customer satisfaction and customer experience even inside debt collection conversations that have historically felt adversarial and it is exactly the kind of customer behavior insight that turns generic collection strategies into cohort-specific playbooks.

Why Speech Analytics Is the Quiet Recovery Multiplier

If borrower-facing AI agents are the engine, conversation analytics is the gearbox. Speech analytics quietly protects every point of recovery uplift the framework generates.

- Profanity detection flags inappropriate language across 100 percent of calls, not the 5 percent that QA can sample manually.

- Risk mitigation surfaces early warning signs of default or fraud before they show up in the DPD report.

- SOP adherence enforces collection guidelines, fair debt collection practices, and regulatory requirements call by call, which matters more than ever in an RBI-regulated environment where collection laws cut across data security, consent, and call-frequency norms.

- Trend and pattern identification uncovers what actually triggers a payment, whether it is a specific phrase, a particular time window, or a channel preference rooted in customer preferences.

Compliance failures are a hidden tax on recovery. Every penalty, every reputational hit, and every escalation pulls collectors away from accounts that would have paid. AI-led conversation analytics keeps that tax close to zero while feeding the engagement engine fresh signals, with the same observability extending to debt collection services run by third-party debt collection agencies, in-house collection agencies, and recovery partners. The result is consistent debt collection practices across every channel, every script, and every conversation which is what regulators increasingly expect from any AI-augmented debt collection operation.

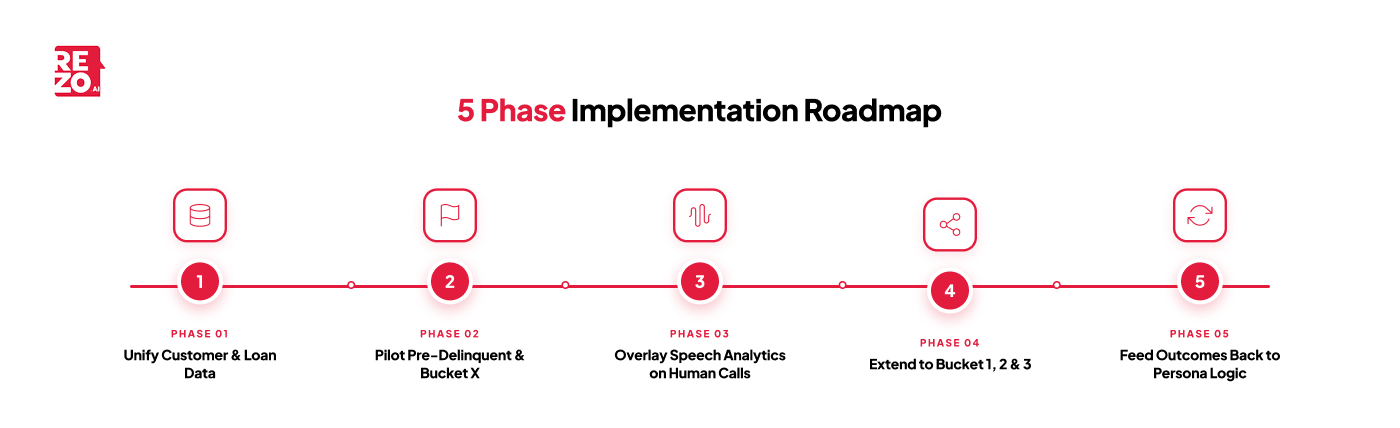

How to Roll This Out Without Disrupting the Floor

The fastest way to lose a debt collection transformation is to switch the floor over in a single weekend. Rezo's typical rollout for an automated debt collection program runs in five phases.

- Data foundation. Unify customer data, loan attributes, bounce count, credit history, CRIF score, and historical conversation transcripts into a single feed, with data security and consent controls wired in from day one. Without this, persona logic underperforms.

- Pre-delinquent and Bucket X pilot. Start where the risk is lowest and the win rate is highest. These buckets absorb 60-70 percent of easy wins from unpaid accounts and prove the connect-rate uplift quickly.

- Conversation analytics overlay. Run AI-led speech analytics on existing human calls in parallel. This surfaces SOP gaps and gives the team a clean baseline before broader rollout.

- Extend to Bucket 1, 2, and 3. Layer omnichannel scripting, voicebot iterations, automated reminders, and CIBIL-intimation flows. Re-route human agents to high-complexity settlements where empathy and negotiation still matter; AI handles the 24/7 digital touchpoints while human collection officers manage sensitive escalations.

- Continuous tuning. Feed conversation outcomes back into persona logic via Rezo's data lake. Recovery curves stop being annual conversations and become weekly ones.

This shape works because every phase is reversible and measurable. A CX or recovery head can hold the floor accountable for one bucket at a time, while the platform compounds learning in the background.

What This Looks Like in the Numbers

The 40 percent uplift in recovery rates is not a hopeful average. It compounds from a sequence of well-understood operational improvements that a digital-first, persona-led debt collection process produces:

- A meaningful lift in right-party contact rates, because outreach is timed and channelled to the borrower's actual preference rather than the dialer's default order which directly translates into stronger cash flow for the lender and a shorter debt collection cycle overall.

- Lower operational costs per recovered account, because high-volume, low-complexity outreach shifts to AI agents while human debt collectors focus on negotiation-heavy buckets. Automated tools and modern debt collection automation have driven 8x faster operations and 2–4x growth in collector productivity in well-instrumented deployments.

- Faster self-cure in pre-due and Bucket X, because the right vernacular nudge reaches the borrower before lapse closing the loop earlier in the collection cycle, reducing bad debts, and helping improve cash flow without escalation.

- Stronger compliance hygiene, because every call is analysed rather than the 5 percent that QA can sample manually; a posture that aligns with both RBI norms and fair debt collection practices globally.

These directionally match what analysts are reporting at the industry level. McKinsey's analytics-enabled collections model points to more than 30 percent savings and threefold increases in monthly installment payments across portfolios when machine learning is wired into the engagement loop. Gartner's forecast on autonomous resolution puts agentic AI on a steep curve through 2029. The gap between industry averages and a well-orchestrated Rezo deployment comes from how tightly the four-step framework is wired into the floor, and how relentlessly the platform iterates on collection strategies week over week. For a wider product view, see how Rezo's collection product is built around this exact loop.

The Path Forward

Debt recovery has stopped being a headcount question. It is now a coordination question, and the platforms that win are the ones that make every conversation smarter than the last. Rezo's Unified CX Agentic AI Platform was built for exactly that, with AI agents that automate omnichannel and multilingual borrower engagement on one side, and AI agents that analyse conversations for insight on the other, all wired into a single stack: turning fragmented collection efforts into a single, learning system that compresses bad debts before they accrue.

If your debt collection operation is still measuring success in dials per agent rather than recovery per cohort, the shift is overdue. The 40 percent uplift is not the headline. It is the floor of what a well-orchestrated agentic AI platform can do across the DPD curve and what mature collection strategies inside large debt collection agencies will increasingly look like by default. To see what this looks like for your own portfolio, explore Rezo's Agentic AI platform or book a walkthrough with the team.

Frequently Asked Questions

Q1: Is AI-led debt collection compliant with regulatory requirements?

Yes. Modern AI debt collections platforms are designed around regulator-aligned guardrails such as RBI fair-practice norms, consent capture, recording retention, and call-frequency caps. Speech analytics enforces SOP adherence on every call, not on a 5 percent QA sample, which lowers compliance risk well below human-led baselines.

Q2: Can AI replace human collections agents entirely?

No, and it should not. AI handles high-volume, low-complexity outreach across pre-due and early DPD buckets, where most accounts self-cure with the right nudge. Human collectors remain essential for late-bucket negotiations, restructuring conversations, and settlement decisions where empathy and judgment drive the outcome.

Q3: What is the difference between traditional and digital-first debt collections?

Traditional debt collections runs on manual dialing, fixed scripts, and limited visibility into borrower behavior. Digital-first debt collections uses persona-led decisioning, multi-channel outreach across voice, chat, email, and WhatsApp, and conversation-level analytics, producing higher connect rates, lower cost per recovered account, and stronger compliance.

Frequently Asked Questions (FAQs)

Take the leap towards innovation with Rezo.ai

Get started now