Why Multilingual Debt Collection Is No Longer Optional in 2026

Why Multilingual Debt Collection Is No Longer Optional in 2026

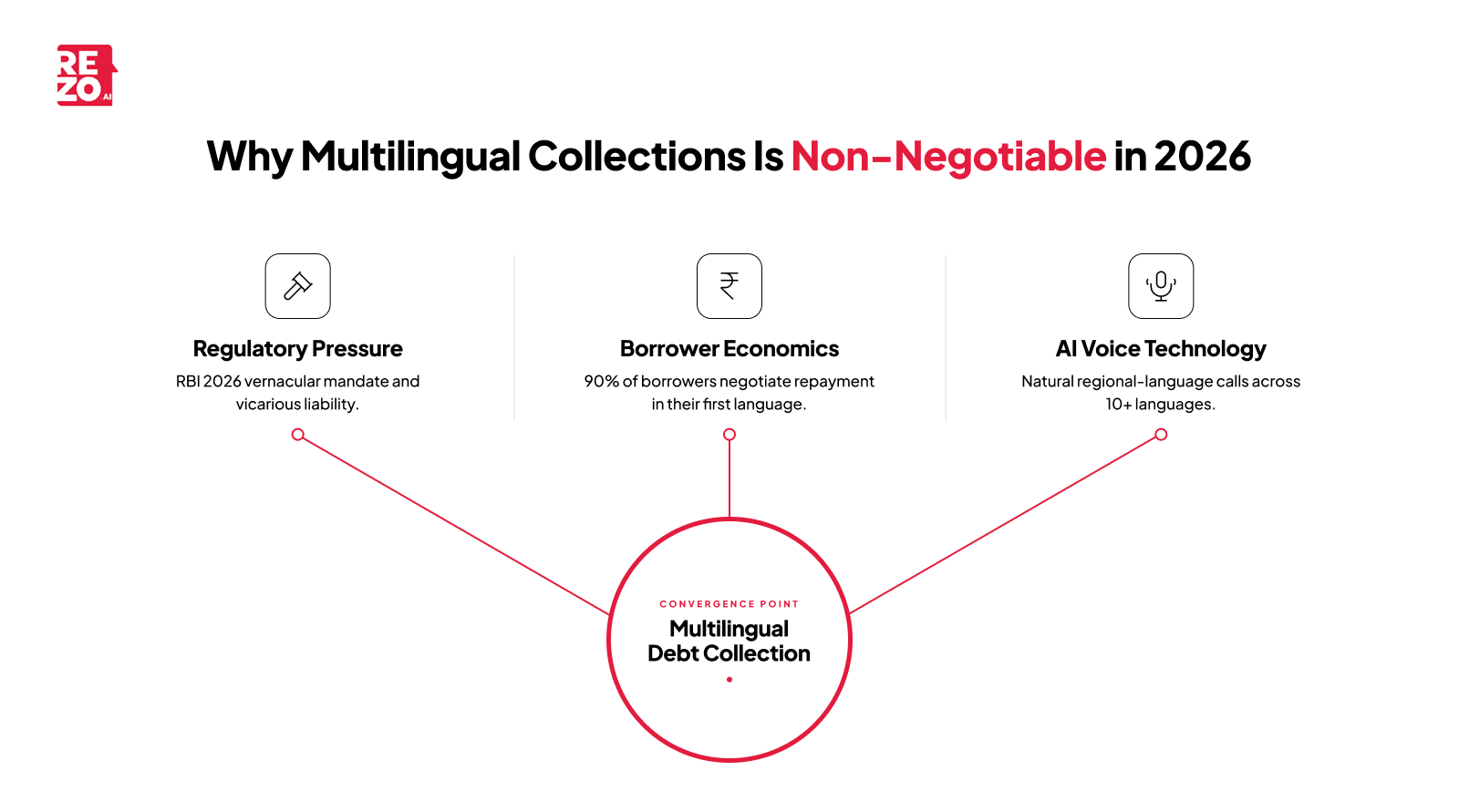

For years, collections teams in India treated multilingual outreach as a "nice-to-have". A few regional-language scripts here, a handful of bilingual agents there, and the rest of the book got the same English template that has powered debt collection call centres for two decades. That arrangement is quietly breaking. Debtors respond measurably better and pay sooner when they are not intimidated by a foreign language, and language barriers are now among the most common reasons debt recovery efforts stall. In 2026, multilingual debt collection sits at the intersection of three converging forces: a tighter RBI rulebook, an undeniable shift in borrower economics, and AI voice agents that finally speak the way Indians actually speak. Lenders who treat language as a peripheral concern are now leaving money, reputation, and regulatory standing on the table.

This article unpacks why the conversation has shifted, what good looks like in 2026, how to roll out multilingual collections without ripping up the existing stack and what Indian lenders can borrow from the playbook of international debt collection services, where meeting debtors in their own language has been standard business practice for decades.

Why the Conversation About Multilingual Collections Has Changed

Walk into any collections war-room today and the contradiction is obvious. The book has grown deepest in tier-2 and tier-3 markets, yet the debt collection language is still tier-1 English. Borrower demographics have shifted faster than collections playbooks. Industry analysis of India's lending growth points to smaller cities and semi-urban geographies as the next wave of credit expansion, where English fluency is far lower than current call scripts assume. Overdue accounts that stall behind language barriers are locked-up cash flow money the business has already lent and now cannot recover on schedule. For banks and NBFCs alike, slow debt recovery is delayed payment at portfolio scale.

At the same time, the RBI has put fresh weight behind borrower-language rights through its 2026 Responsible Business Conduct (Second Amendment) Directions. And AI voice technology has crossed the threshold where regional language calls no longer sound robotic, awkward, or off-script. The result is that multilingual debt recovery has moved from a customer-experience upgrade to a baseline operating requirement for banks, NBFCs, fintechs, and the debt collection agency partners that serve them.

What Is Multilingual Debt Recovery, Really?

Multilingual debt collection is the practice of conducting every meaningful borrower interaction reminder, follow-up, settlement negotiation, dispute capture, hardship conversation in the borrower's preferred language, across voice, chat, WhatsApp, and email. It is not translation. Translation moves words across languages. Multilingual collections moves intent, tone, and trust.

This is the same principle that powers international debt collection around the world. Agencies that recover unpaid debts across borders the heart of international debt recovery have always had to meet debtors in their own language and operate within their local laws. A multilingual international debt collection agency gives its clients legal backing for out-of-court collection avenues in nearly every market. Companies worldwide running international debt collection learned the lesson long ago: an international debt collection agency succeeds precisely because the debtor never has to negotiate in a foreign language. The same holds in commercial debt collection, where unpaid invoices are recovered fastest when the conversation happens on the customer's terms something any company chasing payment across a border learns quickly. Whether the debtors are businesses with unpaid invoices or salaried customers with personal loans, the pattern repeats: money owed gets collected when the debt collection process happens in their language.

A multilingual collections setup also has to handle one of the trickier challenges in Indian lending: the messy reality of how Indians actually speak. Few borrowers stick to "pure" Hindi or "pure" Tamil through a fifteen-minute call. They drift into Hinglish, Tanglish, Benglish. A serious setup is built for that, not against it. The system should switch on the borrower's terms, not its own.

Why English-Only Debt Collection Is Quietly Costing Lenders

The economic argument is the easiest to make, and the one most often missed language is a cash flow problem before it is anything else.

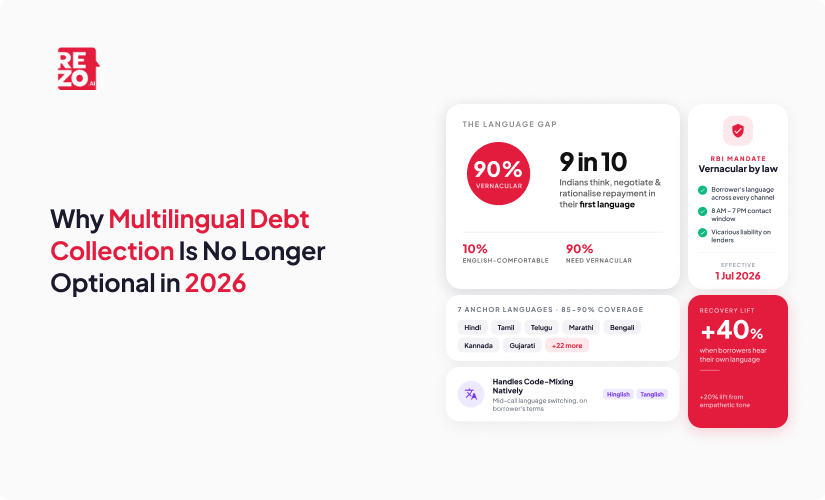

Roughly 15 percent of India is comfortable conducting financial transactions in English. The other 85 percent: your unsecured personal loan portfolio, your two-wheeler book, your gold loan customers, your BNPL exposure is built on customers who think, negotiate, and rationalise repayment in their first language. When the debt collection call opens in English, three things happen at once.

First, connect quality drops. The borrower hesitates, may pretend to understand, or hands the phone to a family member, and the right-party-contact rate slips. Second, comprehension of the payment plan suffers. A borrower who agrees to a restructuring offer they did not fully understand is a borrower who will roll into the next bucket and every roll pushes the account closer to the 90-days-past-due mark where RBI norms classify it as an NPA, converting money the lender could have recovered into bad debt. Third, complaints rise. Misunderstood terms are the single most common root cause of borrower disputes, and disputes consume disproportionate collections capacity and resources. Teams that resolve disputes in the borrower's own language close them in days; disputes handled in the wrong language drag on for weeks.

There is a quieter cost too. Debt collection typically runs in two stages: an amicable first stage, where soft collections focus on preserving the customer relationship and most accounts get paid, and a legal second stage if the account cannot be resolved without legal action. The root cause of non payment is often confusion rather than refusal most debtors will pay the amounts owed once the terms are clear and the ability to pay is matched with a realistic payment arrangement. But when comprehension fails, accounts that should have closed in the first stage of the debt recovery process drift toward escalation. Once a creditor takes legal action, the business economics deteriorate fast: legal proceedings are slow, drain resources, and recovering money owed through a court order takes months. Cross-border and high-value cases may even require debt recovery attorneys and local legal counsel, while straightforward cases handled by an international debt collection agency reach resolution within 4 to 6 weeks when kept amicable; no court order required. That speed is exactly what professional collection services sell. Debt collection experts give clients the same advice: recover early. Successful debt recovery is cheaper, faster, and kinder; every rupee collected amicably costs a fraction of what the same rupee costs afterwards; and most settlement offers land better in the borrower's first language. Language is what keeps accounts at that stage.

Gartner has projected that conversational AI will reduce contact-centre labour costs by roughly $80 billion globally by 2026, and a significant share of that gain in India comes specifically from collections workflows where vernacular automation closes the comprehension gap. Industry analyses point the same way on tone: empathetic communication can enhance recovery rates by roughly 20 percent and empathy is nearly impossible to convey in a language the customer barely follows. The data converges on a simple point: lenders that meet borrowers in their language collect more money, recover it faster, and protect cash flow while doing it a pattern Rezo has documented while delivering 40% higher recovery rates in debt collection for leading NBFC clients.

The Regulatory Why RBI 2026 and the Vernacular Mandate

The Reserve Bank of India has been explicit about borrower-language rights for years. The Fair Practices Code already requires that "all communications to the borrower shall be in the vernacular language or a language as understood by the borrower". RBI guidelines also prohibit threats and abusive language in debt collection a standard that mirrors the Fair Debt Collection Practices Act, the framework that governs how United States debt collectors approach debtors. The pattern is global: localized communications must adhere to regional debt collection acts, and translated scripts must obey each country-specific legal framework. Any international debt collection agency working across jurisdictions already runs these practices as a baseline. What changed in India in 2026 is the enforcement posture.

The Responsible Business Conduct (Second Amendment) Directions, scheduled to take full effect from 1 July 2026, tighten how lenders and their recovery partners interact with borrowers. Communication-window rules are now explicit (8:00 AM to 7:00 PM), including for automated channels. Recovery agents must hold valid IIBF certification. Borrower consent and the right to withdraw it must be captured cleanly.

The clause that often gets missed is vicarious liability. If a third-party debt collection agency, voice bot, or DCA breaches an RBI norm on behalf of its clients, the regulated entity the bank or NBFC is deemed to have committed the breach. The legal exposure cannot be outsourced. A non-compliant non-English call originated by a vendor sits on the lender's compliance ledger, exactly as it would for financial institutions anywhere in the world.

This is where multilingual capability stops being a CX project and becomes a compliance project. Every consent prompt, every disclosure, every escalation note has to be available in the borrower's language. The audit trail has to prove it.

How AI Voice Agents Finally Made Multilingual Collections Practical?

For most of the last decade, "going multilingual" in debt collection meant building regional agent pools. It worked, sort of, but it came with high operational costs, heavy attrition, strained supervisory resources, and QA that was almost impossible at scale. A Hindi caller in Lucknow and a Hindi caller in Patna were graded against the same script in a Bangalore review room, and the supervisor often did not speak the language well enough to catch nuance.

Today voice AI has changed that calculus. Modern voice agents handle 10 or more Indian languages with sub-second latency and natural prosody. They switch languages mid-conversation when the borrower drifts into Hinglish. They sound like a person, not a recording. And critically, artificial intelligence now has the ability to analyze calls for compliance violations in real time, applying the same guardrails, tone monitoring, and QA scoring uniformly across every language which solves the supervisory gap that always plagued regional agent pools. Adoption is following the capability curve: only 11 percent of debt collectors were using AI technologies as of 2023, but around 60 percent were already somewhere on the AI adoption path in the same TransUnion industry survey and the distance between those two groups is where the competitive advantage currently sits.

The downstream effect is operationally significant. Borrowers who hear a clean Tamil opening engage faster. Borrowers who hear their disclosures explained in Marathi are far more likely to commit to a payment plan and honour it debtors pay faster when they understand exactly what they are agreeing to. The same engines send SMS and email payment reminders in the borrower's native language, cutting non payment driven by simple forgetfulness. Research on conversational AI maturity has consistently pointed to language-native AI as the differentiator between deflection-grade bots and resolution-grade agents, and the same logic carries into collections, where resolution rate is the only number that matters. This is the same logic that underpins AI in debt collection and the early voice-led playbooks now standard in voice AI for personal loans.

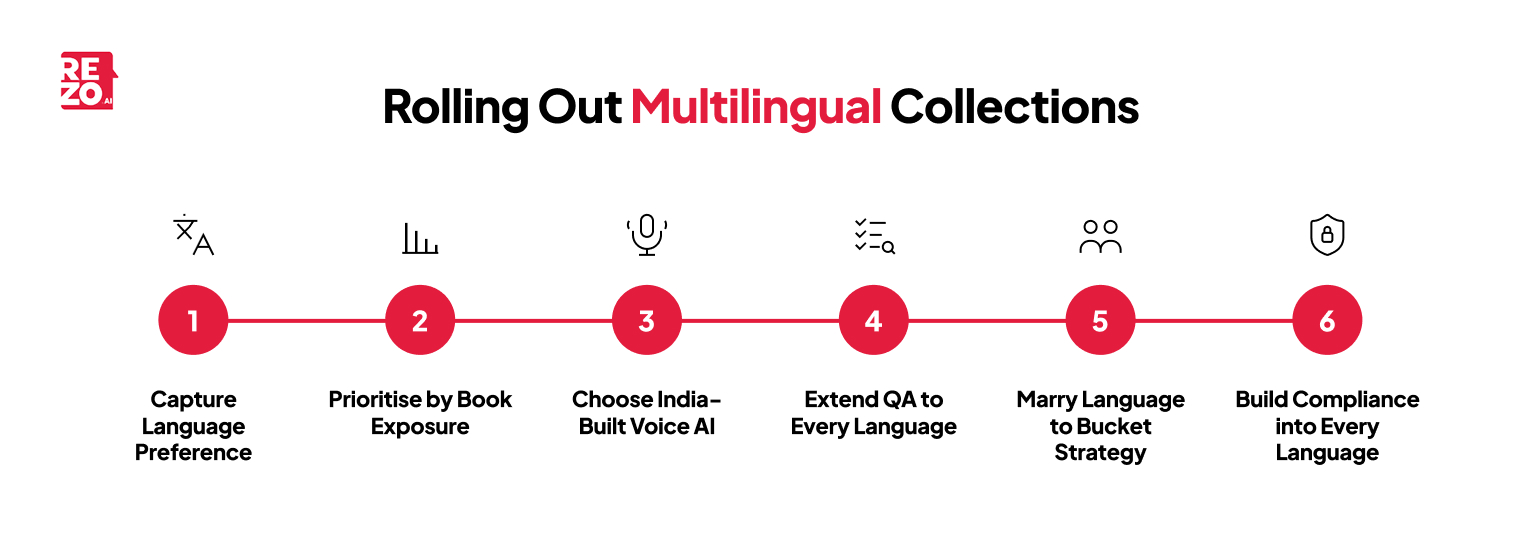

How to Roll Out Multilingual Collections Without Breaking the Stack?

Most of the clients we work with do not need a rip-and-replace. They need a phased rollout that respects the existing book, the existing tech, and the way the debt recovery process already runs — whether collections is handled first party, through a debt collection agency, or via outsourced services. The real challenges are sequencing and data quality, not technology. A practical sequence looks like this.

Phase 1 — Capture language preference as a first-class data field. Most LMS and CRM systems already have it; very few populate it consistently. Treat it with the same discipline as contact details and phone numbers: fix it during the onboarding process, and back-fill from existing voice samples if possible, the way skip tracing back-fills missing contact data.

Phase 2 — Prioritise by book exposure, not by theoretical coverage. No one starts with all 22 scheduled languages on day one. Focus the rollout where your delinquent book actually sits. For most of our BFSI clients in India, the top five or six languages cover 85 to 90 percent of borrower interactions.

Phase 3 — Pick voice AI built for Indian linguistics. A model trained on English and "fine-tuned" for Hindi is not the same as a model engineered for Indic phonetics, code-mixing, and named-entity handling. Clients hear the difference immediately, and it shows up in connect rate within two weeks of rollout.

Phase 4 — Extend QA to every language. A common failure pattern in the QA process is to leave non-English calls unaudited because supervisors do not speak the language. Modern speech analytics scores calls in regional languages with the same rigour as English, and flags edge cases for human review. Use it.

Phase 5 — Marry language to bucket strategy. Persona-led decisioning means a thirty-DPD self-employed borrower in Hyderabad gets a different conversational tone, in Telugu, than a sixty-DPD salaried borrower in Pune in Marathi. Native-speaking teams should still handle high-value or complex accounts where settlement terms and payment plans need nuanced negotiation some clients outsource this layer to BPO firms that specialise in global, multilingual support services and field collections plus skip tracing can be reserved for debtors who genuinely cannot be reached any other way. Language and segmentation work together or not at all.

Phase 6 — Build compliance into every language. Consent capture, do-not-call honouring, communication-window enforcement, and complaint logging must all function natively in the borrower's language and in line with local laws and legal requirements. Treat this as non-negotiable, because the regulator does.

What Good Looks Like: The Markers of a Mature Multilingual Collections Programme?

A short benchmarking checklist for collections leaders evaluating where they stand.

- Borrower language preference is captured at origination and honoured across every channel

- Voice AI handles code-mixing naturally, including handoffs to human agents in the same language the debtor started in

- QA coverage is language-agnostic, with regional-language calls audited at the same rate as English

- Compliance and consent prompts are stored in an audit trail in the borrower's language

- Recovery KPIs (RPC, RTP, kept-promise, roll rate, amounts collected) are tracked by language cohort, not just by region

If three or more of these are not yet true in your environment, multilingual collections is currently a risk in your operation, not a capability.

The Bottom Line: Why 2026 Is the Year This Becomes Non-Negotiable

The three forces have arrived at the same point in the calendar. The regulator now enforces what was previously a guideline. The economics now reward what was previously a courtesy. The technology now delivers what was previously a project plan with no end date.

Lenders who continue to treat multilingual debt recovery as a roadmap item rather than a baseline are accepting a measurable cost on both sides of the ledger. Compliance risk sits with them under vicarious liability. Debt recovery leakage compounds quietly in every tier-2 bucket, cash flow tightens, and unpaid debts age into bad debt money no one ever recovers. And borrower trust, once eroded by a poorly handled non-English conversation, is expensive to rebuild a crucial consideration in a business where customer retention and recovery outcomes rise and fall together.

The collection strategies pulling ahead in 2026 treat language as infrastructure, not as a feature the same shift every international debt collection agency went through years ago, and it applies to consumer and commercial debt collection alike, for large companies and focused NBFCs. Multilingual collections is the floor now. The competitive question is what you build on top of it.

If you are evaluating where your stack sits on this checklist, Rezo AI is built ground-up for India's linguistic reality, with voice, chat, and analytics unified in a single multilingual layer.

Frequently Asked Questions

Q1: Can a borrower in India legally refuse to speak to a recovery agent in English?

Yes. Under the RBI Fair Practices Code, borrowers can insist that all communication happens in a language they understand. Collection agents also cannot use threats or abusive language in India. Lenders have a legal obligation to accommodate both, and a refusal to do so is grounds for an RBI Ombudsman complaint often the fastest way to resolve disputes with a lender.

Q2: How many Indian languages should a collections programme realistically support?

Most lenders and the debt collection services they partner with cover 85 to 90 percent of borrower interactions with five to seven languages. Hindi, Tamil, Telugu, Marathi, Bengali, Kannada, and Gujarati typically anchor the list, with additions driven by the actual geographic spread of the delinquent book.

Q3: Does WhatsApp-based debt collection also need to be in vernacular?

Yes. RBI's communication rules apply across every channel, including WhatsApp payment reminders, SMS, and email. Vernacular obligations and 8 AM to 7 PM contact-window rules cover digital touchpoints, not just voice calls.

Frequently Asked Questions (FAQs)

Take the leap towards innovation with Rezo.ai

Get started now