Why Omnichannel Communication Is Essential in Debt Collections and How Rezo AI Delivers It

Why Omnichannel Communication Is Essential in Debt Collections and How Rezo AI Delivers It

Think about your own phone for a moment. An unknown number rings, and you let it go to voicemail. But a text with a clear payment link? You tap it. That instinct is now shaping recovery, and it explains why omnichannel communication in collections has moved from nice-to-have to non-negotiable. Borrowers screen, block, and ignore calls, yet they happily reply to a message or self-serve through a portal. Meanwhile, delinquency volumes keep rising and patience for intrusive outreach keeps shrinking.

That tension is exactly what omnichannel collections is built to resolve. McKinsey found that digital-first customers make roughly 12% more payments, a clear signal that meeting people where they already are works. Across debt collection and debt recovery alike, omnichannel communication in debt collection is fast becoming the default operating model. This guide covers what omnichannel collections is, why it matters, how to build it, how to keep it compliant, how to measure it, and how Rezo AI delivers it.

What Is Omnichannel Communication in Collections?

Omnichannel communication in collections is a coordinated approach where every channel (voice, SMS, email, WhatsApp, and self-service portals) shares one continuous context, so the conversation moves with the customer no matter where they engage.

The key word is context, not coverage. Plenty of debt collection agencies already use multiple communication channels. What sets omnichannel apart is that those communication channels behave as a single, connected conversation rather than a scattered set of touchpoints. When a borrower starts a payment plan in a chat and later picks up a call, the agent (or the AI) already knows where things stood in the collection process. Nothing is repeated, nothing is lost.

This is where omnichannel is most often confused with something it is not: multichannel.

Also Read: Omnichannel Customer Support

Omnichannel vs Multichannel in Debt Collection: What's the Difference?

Multichannel means many channels operating in silos. Omnichannel means many channels operating as one continuous conversation. The key differences come down to context: think of it as the difference between separate chapters scattered across desks and a single, shared book everyone is reading from.

Picture a customer who opens a self-service portal, abandons mid-payment, then receives a follow-up SMS that already knows exactly where they left off. That continuity, one seamless and consistent experience rather than a jump between multiple platforms, is omnichannel in action.

Also Read: AI in Debt Collection

Why Is Omnichannel Communication Essential in Collections?

Consumer behavior has shifted decisively toward digital-first and self-serve interactions. Voice-only outreach, especially from unfamiliar numbers, increasingly goes unanswered, which means relying on one channel alone leaves money on the table.

The performance gap is measurable. FICO reports that coordinating outreach across communication channels can meaningfully lift customer engagement and the rate at which engagement converts to liquidation. On the portfolio side, experts link digital-first collections models to lower non-performing loan levels and a reduction in the cost of collections, alongside that 12% lift in payments from digital-first customers.

There is also a simple expectation problem. Salesforce research shows the overwhelming majority of customers expect consistent, connected interactions across channels, and roughly 83% expect an immediate response when they reach out. When collections feels disjointed, it stands out for the wrong reasons.

Finally, meeting people on their preferred channel is respectful. It lowers friction, reduces the sense of being chased, and protects the long-term relationship. That customer-experience signal matters, because today's delinquent account is often tomorrow's loyal customer.

Why it matters, in short:

- Digital and self-serve channels reach customers who ignore calls

- Coordinated channels lift customer engagement and recovery rates

- Consistency meets a baseline customer expectation

- Respectful, choice-driven outreach protects the brand

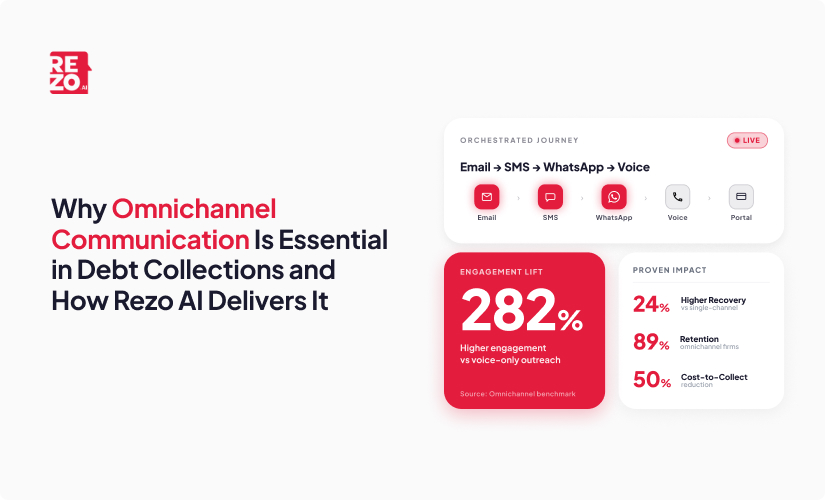

The numbers behind this omnichannel approach are hard to ignore. Debt collection agencies that run coordinated omnichannel strategies report a higher recovery rate than single-channel operations, and an omnichannel strategy can reportedly drive as much as 282% higher engagement than voice-only methods. The retention effect is just as striking: companies with a strong omnichannel strategy retain around 89% of their customers. This is why leaning on one channel, or forcing every borrower down a single channel, quietly caps what you can recover.

Also Read: Multilingual Debt Collection

What Channels Belong in an Omnichannel Collections Strategy?

A strong omnichannel debt collection channel mix usually spans several contact channels:

- Voice for sensitive, complex cases, or high-value conversations, when a phone call is genuinely the right channel

- SMS and text messages for quick nudges, payment reminders, and payment links

- Email for detailed statements, disclosures, and records

- WhatsApp for two-way, conversational engagement

- Web and self-service portals for self-cure payments and making payments at any hour

- Mobile apps and push notifications for automated reminders that surface where borrowers already spend their attention

- Autonomous AI assistants and virtual agents to handle routine interactions at scale

The case for these digital channels and digital tools is behavioral, not theoretical. Consumers increasingly prefer digital self-service options, and Experian found that around one in five online debt resolution sessions occur outside traditional business hours, highlighting the need for always-on collections experiences. Many modern consumers would simply rather tap a link or open a mobile app than take a phone call, and customers prefer to choose for themselves, so the communication methods you offer have to match those diverse preferences. In India and other emerging markets, the mix tilts toward WhatsApp-first engagement, regional language support, and integration with local digital payment rails, all of which dramatically widen reach and help you reach customers a single channel never would.

Also Read: Hyper-personalisation in Debt Collection

How Does AI Orchestrate the Right Channel at the Right Time?

This is where omnichannel stops being a list of channels and becomes intelligent. AI looks at each customer's behavior and response history to predict the best channel, the best time, and even the right tone for the next outreach. Predictive analytics and machine learning read previous interactions and payment behavior to decide the next move, so someone who always replies to evening text messages is treated differently from someone who only engages through a portal on weekends. Tone appropriate messages, matched to debtor behavior and each debtor's preferences, keep the conversation human even when it is automated. This is what effective communication looks like at scale.

Just as important is the handoff. AI carries context across multiple channels, so a customer never has to repeat themselves when they move from a chatbot to a live agent or from email to voice. Those seamless transitions between channels are what turn a set of contact channels into one connected experience, and they are the difference between scattered communication strategies and a single coordinated one.

Conversational automation also does the heavy lifting on routine cases, balance checks, automated reminders, and simple payment plans, which frees human agents for the sensitive accounts where empathy and judgment count most. It also lets teams scale outreach efficiently without adding staff. And because the model keeps learning from what actually drives promise-to-pay, channel sequencing gets sharper over time.

Personalized communication is a large part of why this works. Epsilon research found that 80% of consumers are more likely to do business with a company that offers personalized experiences, and in collections that personalization improves both customer satisfaction and trust. When personalized messages reflect a borrower's real situation, they can increase payment arrangements significantly as compared with generic reminders.

A typical orchestration journey looks like this: a gentle email nudge, followed by an SMS reminder if there is no response, then an invitation to self-cure through the portal, and finally a human or AI voice call for non-responders. Each step is informed by the last.

AI debt collection turns a scattergun of messages into a guided path tailored to each borrower.

How Do You Build an Omnichannel Collections Strategy? (Step-by-Step)

You do not need to boil the ocean. A clear, sequenced rollout works best, and these key strategies keep it manageable:

- Audit your current communication channels, data sources, and the exact points where context breaks today. You cannot fix handoffs you cannot see.

- Unify data into a single customer view that connects your CRM systems, payment systems, and communication tools, so every channel reads from the same record as one integrated system.

- Segment customers by risk, behavior, and preferred channels, because a self-curing borrower and a hardship case need very different journeys.

- Sequence channels intelligently, for example email to SMS to self-service portal to voice for non-responders, rather than blasting every channel at once.

- Automate and orchestrate with AI so handoffs preserve context and the right channel fires at the right moment.

- Measure and optimize against clear KPIs, then feed those learnings back into your sequencing (more on this next).

Common pitfall: legacy-system integration is where most omnichannel programs stall. Data trapped in disconnected platforms recreates the very silos you are trying to remove, so prioritize a unified data layer early rather than bolting it on later.

This is the practical answer to how to build an omnichannel strategy: connect the data, then orchestrate the journey so your whole contact strategy can leverage digital communication instead of fighting it.

Also Read: Predictive Analytics in Debt Collection

How Does Omnichannel Collections Stay Compliant?

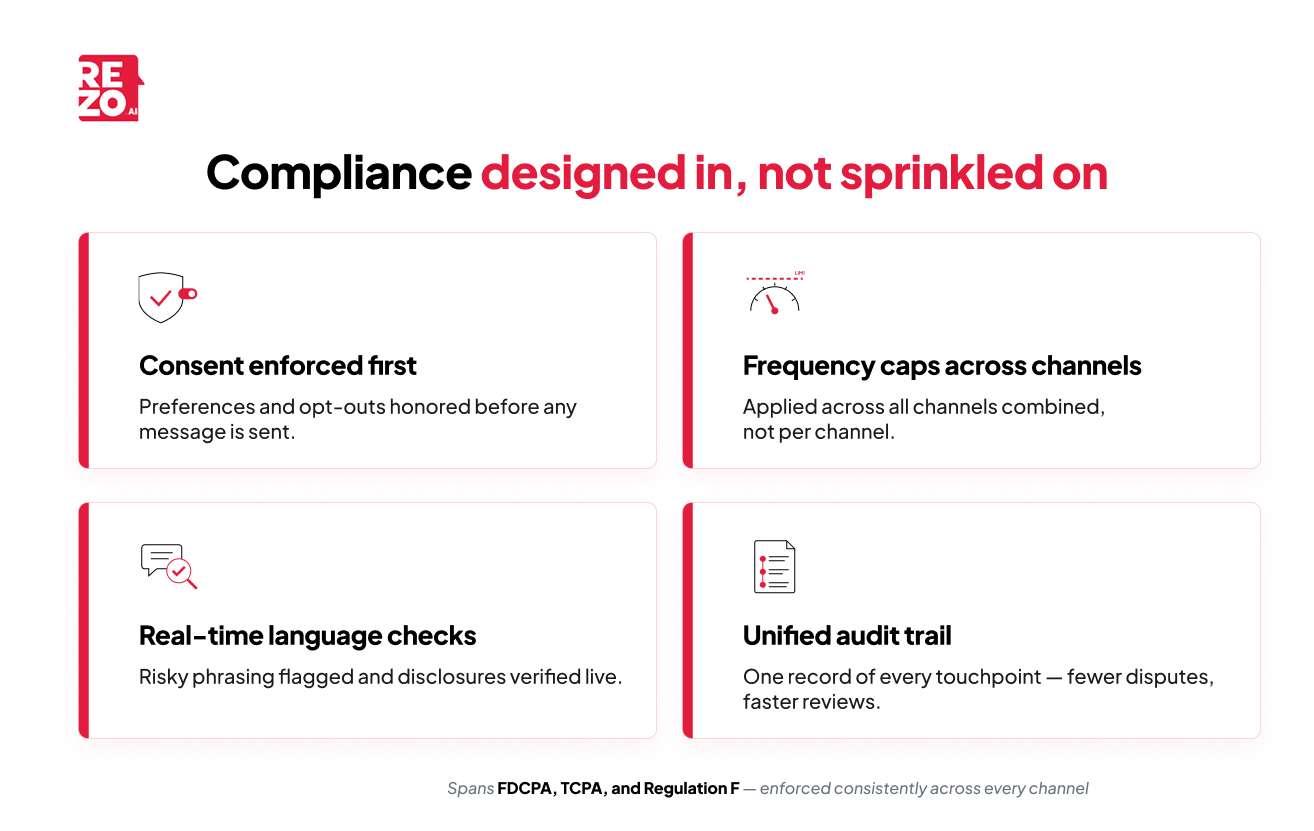

Compliance cannot be an afterthought sprinkled on at the end. It has to be designed into the orchestration itself.

In regulated markets, frameworks like the FDCPA, TCPA, and the CFPB's Regulation F set the guardrails for contact frequency, channel consent, and required disclosures, and local regulations vary by region. An omnichannel debt collection system has to respect those rules and regulatory compliance consistently across every channel, not just one.

The good news is that the same intelligence that orchestrates channels can enforce compliance in real time. AI can flag risky language, hold outreach within contact-frequency limits, honor explicit consent and opt-outs, protect sensitive data, and maintain a complete audit trail of every interaction. Automated workflows and centralized data make this consistency far easier to sustain, and by removing duplicate or mistimed outreach they measurably reduce compliance risk.

Compliance built into the design looks like:

- Consent and channel preferences enforced before any message is sent

- Frequency caps applied across all channels, not per channel

- Real-time language and disclosure checks on automated and live conversations

- A single, unified audit trail that reduces disputes and speeds reviews

That last point is the quiet advantage of omnichannel collections compliance: one consistent record of every touchpoint is far easier to defend than fragments scattered across systems.

How Do You Measure Omnichannel Collections Success?

If you want to know whether your omnichannel debt collection effort is working, watch a focused set of performance metrics rather than vanity numbers. Key indicators include:

- Right-party contact rate, are you actually reaching the customer

- Channel response rates, which channels earn replies

- Promise-to-pay rate, and how many promises convert

- Self-cure and self-service adoption, the share resolving without an agent

- Cost-to-collect, tracked as one efficiency metric among several

- Complaint rate and channel opt-out rate, your customer-experience guardrails

Read together, these tell you not just whether you are recovering more, but whether you are doing it in a way customers tolerate. The payoff is real: mature omnichannel and analytics programs have been shown to cut the overall cost to collect, largely by shifting late payments to self-service and letting real-time analytics guide every decision. Yet many teams still never adjust their channel strategy based on how customers actually respond, which leaves that upside on the table. Feed the results back into your sequencing, and the loop tightens with every cycle. That is how to measure omnichannel collections success in practice.

How Rezo AI Delivers Omnichannel Communication in Collections

Rezo AI brings all of this together in one place. It unifies voice, chat, SMS, WhatsApp, and self-service into a single orchestrated, context-aware conversation, so the customer experience stays continuous no matter how a borrower chooses to engage. Instead of stitching together multiple platforms, teams get one of the few genuinely unified omnichannel platforms built for debt collection and recovery.

The platform uses Agentic AI and Data Analytics to select the right channel, time, and tone for each customer, and it hands off context seamlessly between automated assistants and human agents. Nobody repeats themselves, and agents step in already knowing the full picture. Two-way customer interactions, personalized messages, and consistent messaging across every channel are what lift response rates and boosts engagement, delivering the kind of seamless interactions and consistent experience that keep the customer's attention. Behind the scenes, the same data and past interactions quietly sharpen the next contact.

Compliance is built in, with real-time monitoring and a unified audit trail spanning every channel, so consistency and defensibility come standard rather than as an extra project. And because it is designed for high-volume, multilingual, multi-channel operations, it fits the realities of BFSI, lending, and collections teams managing huge interaction volumes across regions and languages.

The Bottom Line

Collections is no longer a series of disconnected calls. It is a single conversation that follows the customer across whichever channel they prefer, carrying context the whole way. Done right, omnichannel communication in collections lifts engagement and recovery, protects your brand, and stays compliant by design rather than by luck. The shift in borrower behavior is not slowing down, so the debt collection agencies that orchestrate channels intelligently will keep pulling ahead of those still relying on the ring of an ignored phone.

Frequently Asked Questions

What is the most effective channel for debt collection?

There is no single best channel. Effectiveness depends on each borrower's preference and behavior. Digital channels like SMS and WhatsApp see high response rates, while a voice phone call still suits sensitive cases and negotiating payment plans that need a human touch. The strongest results come from matching the channel to the individual customer.

How long does it take to implement an omnichannel collections system?

Timelines vary by data readiness and system complexity, typically ranging from a few weeks to several months. The biggest factor is integrating legacy systems into a unified data layer. A phased rollout, starting with core channels, lets teams see value faster.

Is omnichannel debt collection more expensive than traditional methods?

Not over time. Upfront integration costs exist, but automation, higher self-cure rates, and better debt recovery lower the overall cost-to-collect. Digital and self-service channels reduce reliance on manual phone calls, often making omnichannel more cost-efficient than voice-only collections.

Frequently Asked Questions (FAQs)

Take the leap towards innovation with Rezo.ai

Get started now